Intel Corporation INTC recently announced the immediate retirement of CEO Pat Gelsinger, with David Zinsner and Michelle Johnston Holthaus being named as the interim Co-CEOs of the company. The corporate restructuring of the top management was aimed at reviving the lost glory as Intel fell down the pecking order to relinquish its coveted position on the Dow Jones Industrial Average (“DJIA”) to NVIDIA Corporation NVDA.

The radical shakeup in the leading stock market index marked a significant shift in the semiconductor ecosystem with the growing dominance of AI (artificial intelligence) and ended Intel’s 25-year run in DJIA. Before the board could zero in on the new CEO to steer the ship, the top management offered a sneak peek at the broader goals of the company to soothe investor sentiments.

INTC’s Core Strategy Remains Unchanged

Dispelling concerns regarding any knee-jerk reactions, management vouched that the core strategy of the company would remain unchanged and reiterated its earlier revenue guidance of $13.3-$14.3 billion for the fourth quarter of 2024. The company aimed to emphasize the diligent execution of operational goals to establish itself as a leading foundry.

However, management observed that the company needs to witness a significant cultural change to transition from Integrated Device Manufacturing to being a world-class foundry. This would involve a shift from a “no wafer left behind” mindset, where the company built extra capacity to meet demand (hoping that the added capacity would not be idle at any time) to “no capital left behind” mindset that aims to drive efficiency by eking out every wafer possible from the existing capacity.

INTC Betting Big on AI Chips

Intel has launched AI chips for data centers and PCs. This marks one of the largest architectural shifts for the company in 40 years. The strategic decision is aimed at gaining a firmer footing in the expansive AI sector, spanning cloud and enterprise servers to networks, volume clients and ubiquitous edge environments, in tune with the evolving market dynamics.

The company has unveiled the Intel Core Ultra, which features a neural processing unit that enables power-efficient AI acceleration with 2.5x better power efficiency than the previous generation. With superior GPU and CPU capabilities, it can speed up AI solutions. The company also launched the new vPro platform with Intel Core Ultra processor that delivers enhanced power efficiency. With dedicated AI acceleration capability spread across the central processing unit, graphics processing unit and the new neural processing unit, it will unlock an endless new wave of AI experiences across all apps.

Intel Lagging on Innovation?

Although Intel has scaled its AI footprint, it lagged NVIDIA on the innovation front, with the latter’s H100 and Blackwell graphics processing units (GPUs) being runaway successes. Leading technology companies are reportedly piling up NVIDIA’s GPUs to build clusters of computers for their AI work, leading to exponential revenue growth.

An accelerated ramp-up of AI PCs further affected the short-term margins of Intel as it shifted production to its high-volume facility in Ireland, where wafer costs are typically higher. Margins were also adversely impacted by higher charges related to non-core businesses, charges associated with unused capacity and an unfavorable product mix.

Intel has been facing challenges due to the disruptive rise of over-the-top service providers in this dynamic industry. Price-sensitive competition for customer retention in the core business is expected to intensify in the coming days. Aggressive competition is likely to limit the ability to attract and retain customers and affect operating and financial results.

Image Source: Zacks Investment Research

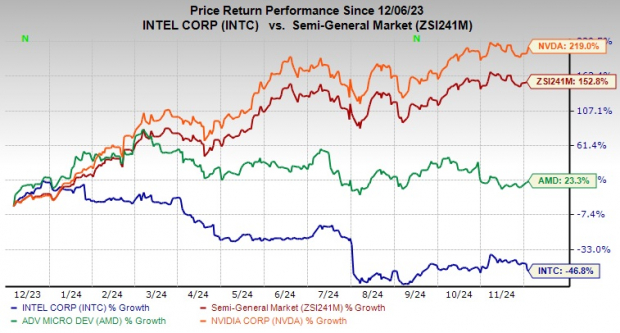

INTC Stock Price Performance

The stock has plunged 46.8% in the past year against the industry’s growth of 152.8%, lagging its peers Advanced Micro Devices, Inc. AMD and NVIDIA. Much of this underperformance is due to severe financial difficulties and operational challenges, which have forced management to undertake a comprehensive review of its businesses.

Intel is mulling various options, including the potential split of its product design and manufacturing divisions and evaluating which factory projects should be terminated. It also plans to establish Intel Foundry as an independent subsidiary to unlock strategic benefits and improve capital efficiency with clearer separation and independence from the rest of Intel. The division incurred an operating loss of $5.8 billion in the last reported quarter.

INTC Stock One-Year Price Performance Comparison

Image Source: Zacks Investment Research

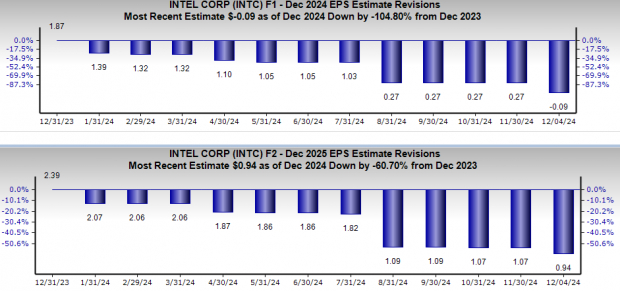

Earnings Estimate Revision Trend of INTC

Earnings estimates for Intel for 2024 have plunged 104.8% over the past year to 9 cents, while the same for 2025 has declined 60.7% to 94 cents. The negative estimate revision depicts bearish sentiments for the stock.

Image Source: Zacks Investment Research

End Note

Intel’s innovative AI solutions hold immense promise for the broader semiconductor ecosystem. By addressing the challenges of scalability, performance and interoperability, it is paving the way for widespread AI adoption across enterprises worldwide. Management is focusing on simplifying parts of its portfolio to unlock efficiencies and create value. It has aimed to allay investor concerns by reiterating its short-term guidance while maintaining core focus.

However, the recent product launches appear “too little too late” for Intel. In addition, margin woes amid strict export restrictions, unfavorable product mix and elevated customer inventory levels weigh on its bottom line. With declining earnings estimates and abysmal price performance compared with its peers, the stock is witnessing a negative investor perception. With a Zacks Rank #3 (Hold), Intel appears to be treading in the middle of the road, and investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Intel Corporation (INTC) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.