There’s a very specific kind of magic that happens when you’re doing your taxes and the number in red suddenly flips to green.

You know the one I mean. One second, the screen is telling you that you owe the IRS $500. The next? You’re staring at a refund. A real, actual refund. Something we hadn’t seen in our household in years.

My husband and I just sat there blinking.“Did that really just happen?”

It did. And the reason was my home office.

To be clear, this wasn’t some sketchy tax trick or loophole I saw on TikTok. This was alegitimate deduction available to self-employed folks who regularly and exclusively use part of their home for business. I’d started doing more freelance editing and writing over the last few years and had set up an LLC both for liability reasons and, frankly, as a personal finance experiment.

I figured I’d be able to write off obvious business expenses — things like the computer software I used, my laptop, maybe even a new desk chair. But what I didn’t realize is that I could also deduct a percentage of my utilities. My internet bill. My pest control. Even the cost of the housekeeper who cleans that room.

All of it.

And it added up to over a thousand dollars in tax savings.

This is the story of how my home office — the same one I use to file invoices, write articles, and host Zoom calls with no fewer than three coffee mugs on my desk — ended up being one of my favorite tax wins of the year.

And because I genuinely like you — you’re taking the time to read my article, of course I like you — and want you to get every dollar you’re entitled to, I’m going to let you in on what I’ve learned. I had no idea how valuable this deduction could be until I dug into the details myself. So if it can help you too? Even better!

The IRS Has Rules — Here’s How to Make Sure You Qualify

I want to be really clear about this upfront because the IRS is very specific about what qualifies — and what doesn’t.

To take the home office deduction, you have to meet two main requirements:

Exclusive Use: The space must be used exclusively for business. That means no dual-purpose rooms. If your guest room also doubles as your Zoom background, sorry — that’s not going to cut it. It has to be a space that’s set asidespecifically for work.

Regular Use: You also need to use the space regularly for your business. Not just once a month when inspiration strikes or when the living room is too loud. It needs to be yourconsistent work location.

The space doesn’t need to be a whole separate room, but it does need to be a clearly defined area that meets both of those conditions. So yes, if you’ve carved out a dedicated desk nook where you run your side business — and you use it exclusively and regularly — it might qualify.

Also important: This deduction is only available to self-employed individuals. If you’re a W-2 employee working from home, even full-time, this doesn’t apply to you. (Sorry — I don’t make the rules. But maybe it’s worth bringing up with Congress.)

When I first started my LLC, I didn’t know most of this. I’d heard the phrase “home office deduction” thrown around before, but I assumed it was only for people who ran full-blown businesses out of their houses — not someone like me who occasionally worked from the kitchen table, the couch, or wherever the toddler chaos wasn’t.

It wasn’t until I sat down to do our 2023 taxes — the first year my LLC was fully up and running — that I started looking into what actually went into the various self-employment deductions. I learned about the regular and exclusive use requirements, and it clicked. “Oh, this deduction isn’t just for people with fancy home studios… It’s for anyone running a legit business who’s willing to carve out the space.”

So I made some changes. We had a spare downstairs room that wasn’t being used for much — a sort of accidental sitting room that no one ever sat in. It was quiet, had a door, and just so happened to be the perfect size. So I claimed it. I moved in my desk, set up shop, and made it my dedicated office space.

By the time we hit 2024, I had a fully qualified home office — and a whole new appreciation for how productive (and tax-efficient) a single room could be.

How I Turned a Random Room into a Legit Tax Deduction

My home office is approximately 280 square feet, which shakes out to just over 9% of our total home. That means I get to deduct 9% of eligible household expenses — things like our electricity, internet, and homeowners insurance — because those things support my work and my workspace.

Now, the IRS gives you two ways to calculate your deduction:

– The Simplified Method, which is just $5 per square foot (up to 300 square feet). So, for my 280 sq. foot office, I could’ve just claimed a flat $1,400 and called it a day.

– The Regular Method, which is what I chose. This method takes a little more work (you fill out Form 8829), but it lets me deduct a percentage of actual expenses for things like utilities, insurance, repairs, pest control, housekeeping — and even depreciation on the house.

That part is wild. We usually take the standard deduction on our taxes, which means we don’t get to itemize things like mortgage interest or real estate taxes.

But with the home office deduction, we get to carve out just the portion of those expenses that applies to my workspace. So even though we’re not itemizing on our main return, we still get to deduct a portion of our mortgage interest and property taxes — just for the home office.

I think I had to read that part three times before it clicked. But yep — it’s allowed.

Electricity? Internet? Pest Control? Yes, You Can Probably Deduct That

Before we go any further, let me just say this loud and clear: I am not an accountant.

If you’re thinking about taking the home office deduction, please talk to a qualified tax professional. This article is just me, a finance nerd, sharing my own experience and what I learned along the way.

Okay? Okay. Let’s get into the good stuff.

If you use the regular method for the home office deduction — which is what I did — you essentially get to split certain home expenses between personal and business use, based on how much of your home you use for work.

For me, that’s about 9% of our home. My office is 280 square feet, and that’s enough to qualify for a pretty meaningful slice of expenses I was already paying.

Here’s how it breaks down:

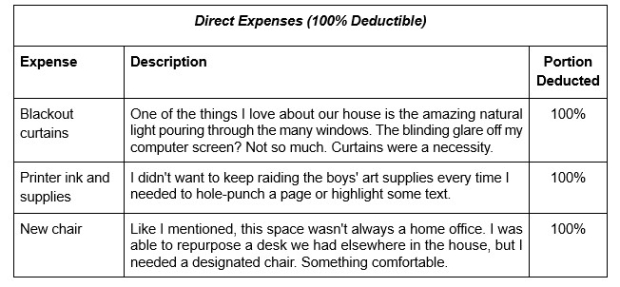

Fully Deductible “Direct” Expenses

These are costs that apply only to your office. For example, I installed blackout curtains in my office to help with Zoom lighting. Because those curtains only benefit the office, that’s considered a direct expense — and that cost is 100% deductible.

Same goes for things like:

– Office-specific repairs (e.g., fixing the door, replacing carpet)

– Painting the walls in your office

– A separate business-only phone line

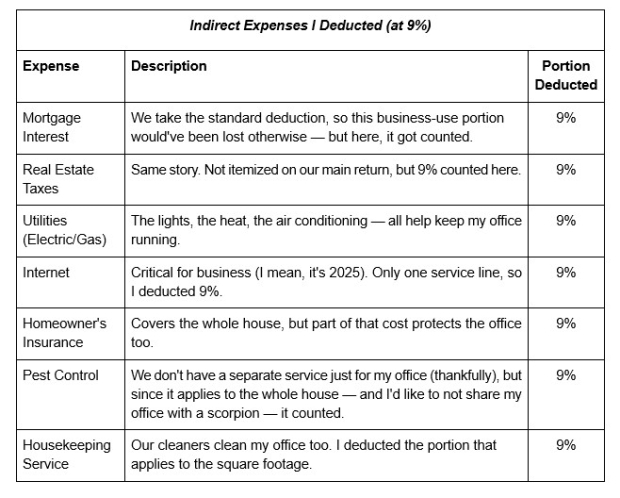

Partially Deductible “Indirect” Expenses

These are costs that apply to the entire house, but since your business is benefiting from a portion of them, you can deduct a percentage. In my case, that means 9% of:

– Mortgage interest

– Real estate taxes

– Electricity and gas

– Internet

– Homeowner’s insurance

– Pest control

– Cleaning services

All of those became indirect home office expenses. And this is where things get interesting.

Because we normally take the standard deduction, we don’t itemize our mortgage interest or property taxes. But when you use the regular method for your home office, you do get to deduct the business-use portion of those costs, even if you’re taking the standard deduction on the rest of your return.

That means I got to write off a piece of my mortgage interest and property taxes that would otherwise just be… nothing. They don’t count toward our standard deduction, and they don’t help us in any other way. But thanks to the home office deduction, they did help — and reduced our taxable income in the process.

(And because that’s a business deduction, not an itemized one, it also helped lower the amount of self-employment tax I had to pay. Bless.)

Peek Inside My Deduction List — and What Surprised Me

When I sat down to calculate everything, I was shocked by how quickly the deductions added up. A few percentage points here and there doesn’t sound like much… until you realize you’re applying that percentage to your biggest recurring bills.

Here’s a snapshot of what I deducted — using the regular method, and based on 9% business use of my home:

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Direct expenses were rarer for me — but anything that applies only to the office is fully deductible. And, of course, these are just the expenses that apply to my home office and my work. What I deduct will likely look very different than what someone else deducts.

One important distinction: If I had purchased a separate business insurance policy (or rider for my LLC), that wouldn’t be part of the home office deduction. It’d be a fully deductible business expense elsewhere on my Schedule C. (Again: accountant. Talk to one.)

One more detail worth noting: If you’re only using your home office for part of the year — for example, you started freelancing in July — you’ll only be able to deduct expenses for that portion of the year. The IRS doesn’t let you claim a full year of deductions for a six-month business. So timing matters.

How My Tax Bill Went From Red to Green in One Click

When I hit “enter” on the last batch of expenses, I wasn’t expecting fireworks.

I was just hoping to knock a couple hundred bucks off our total tax bill. Maybe ease the sting a little. What I didn’t expect was to see our entire tax situation flip.

One second, we were staring at a $500 payment due. The next, we were getting a refund.

And to be clear, this wasn’t magic. It was math. Boring, spreadsheet-driven math — the kind that takes a while to input and even longer to double-check. But when it worked… wow, did it work.

That was the moment it hit me: This deduction wasn’t just about saving a few bucks on office supplies. It was about treating my business — and my time — like it matters.

I was already paying for electricity. Already paying for the internet. Already paying for pest control and a housekeeper. Nothing about my life changed — except the fact that now, some of those unavoidable costs were working for me.

And as someone who’s filed taxes as a W-2 employee for most of my life, I can’t overstate what a mental shift this was. For the first time, I felt like I wasn’t just on the hook for taxes — I was finally getting to play by a different set of rules.

Still the same laws. Still fully above board. But this time, I actually got to use them.

Is the Home Office Deduction Worth It? Here’s the Honest Answer

Okay, so, here’s the part everyone reading actually cares about — is claiming the home office deduction actually worth the time and trouble?

This is personal finance! So obviously, the answer is… it depends.

It isn’t worth the hassle if…

– You’re a W-2 employee working from home (unfortunately, employees aren’t eligible for this deduction).

– You occasionally answer emails from your couch and call it a day.

– Your “office” is also your guest bedroom, your treadmill room, and your dog’s nap zone.

– Really any scenario that means you don’t meet the “exclusive and regular use” requirements the IRS lays out.

But it is worth exploring if…

– You’re self-employed, freelance, or run a business from your home — and that business makes enough income to warrant paying attention to taxes in the first place.

– You’ve got a space in your home that’s used only for work and is used that way consistently.

– You’re already paying out of pocket for things like internet, insurance, utilities, and more — and you’d like to turn a portion of those costs into tax-deductible business expenses.

– You’re taking the standard deduction on your taxes and want a way to still benefit from your mortgage interest and property taxes.

If that’s you? Then it might be worth taking the time to understand how this works.

And again — I’m not a CPA. Please do not take this as professional tax advice. This is just one personal finance nerd trying to share something new that unexpectedly saved me $1,000. And even if the home office deduction doesn’t apply to you, still take this as encouragement to ask better questions, talk to your accountant, and dig into what the tax code actually allows.

Because tax deductions aren’t just lines on a form. They’re a way to finally let your money — and your work — pull their financial weight.

Make the Most of Your Money with Professional Insights

Would you like practical tips and tools to help you navigate today’s economy? Zacks’ free Money Sense newsletter cuts through the jargon and gives you actionable tips to help you save money, slash taxes and build a lasting legacy.

From must-see investment ideas to practical budgeting strategies, Money Sense can help you grow your wealth intelligently. Subscribe today and start achieving your next financial goal! It’s absolutely free to sign up.

Get Money Sense absolutely free >>

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.