Key Points

-

Nvidia still can’t keep up with demand for its data center GPUs.

-

After a tepid stock performance in 2025, Amazon is looking to bounce back in 2026.

-

Broadcom’s custom AI accelerator chips are growing in popularity with hyperscalers.

- 10 stocks we like better than Nvidia ›

Although we’re nearly at the end of a year during which the S&P 500 gained a strong 16%, there are still plenty of stocks that look like top-tier buys. Some of the biggest names in the market have retreated from their recent highs, and I think investors should consider scooping them up before 2026 arrives. At the top of my last-minute shopping list are Nvidia (NASDAQ: NVDA), Amazon (NASDAQ: AMZN), and Broadcom (NASDAQ: AVGO).

Image source: Getty Images.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Nvidia

Nvidia has been the poster child for the artificial intelligence (AI) buildout since it began. Its graphics processing units (GPUs) provide the computing power for the vast majority of AI workloads today, but investors are worried about two things.

First, they are concerned that there is a general bubble in the AI space. However, with all of the hyperscalers having announced that 2026 will be another year of record-setting capital expenditures, I don’t see that thesis as valid. Second, some are worried that Nvidia’s dominance in the AI accelerator chip niche is slipping. While there have been several promising product launches from its competitors, Nvidia’s GPUs are still the top option. In its earnings release for its fiscal 2026 third quarter, which ended Oct. 26, CEO Jensen Huang stated that the company is “sold out” of cloud GPUs.

This is a company that brought in $57 billion in revenue during Q3, and it’s clear that it could have made more if it had more chips to sell, so it’s hard to say Nvidia’s dominance is slipping with a straight face.

With Nvidia’s stock price down nearly 20% from its all-time high and Wall Street analysts expecting the chipmaker’s revenue to grow by 48% next year, I can think of few better buys heading into 2026.

Amazon

Amazon stock is essentially flat for the year. However, some recent events have me bullish about it as we prepare to enter 2026.

First, its cloud computing unit, Amazon Web Services, delivered 20% revenue growth rate in Q3 — its best rate in years — showing that it’s resurging as the go-to place to bring workloads online. Second, growth in Amazon’s advertising service business is also reaccelerating. This segment has become a major part of the company’s business over the past few years.

I think Amazon’s stock will come roaring back in 2026, and it will be on the backs of these two important business units.

Broadcom

Broadcom is up by an incredible 40% or so year to date. However, it was previously even higher: The stock sold off heavily after a poorly received earnings report.

In its fiscal 2025 fourth quarter, which ended Nov. 2, revenues grew by 28% as diluted earnings per share (EPS) rose 37%. Its AI semiconductor business was a bright spot, with revenue rising 74% year over year. Management expects this trend to continue into Q1, forecasting that its AI semiconductor revenue will more than double. That all sounds impressive, but the stock sold off in part due to revenue timing.

Broadcom told investors that some of its customers wouldn’t be purchasing some of their custom AI chips until 2027 and beyond. That was a letdown for investors, and many headed for the exit. As a result, Broadcom’s stock is down by more than 20% from its all-time high.

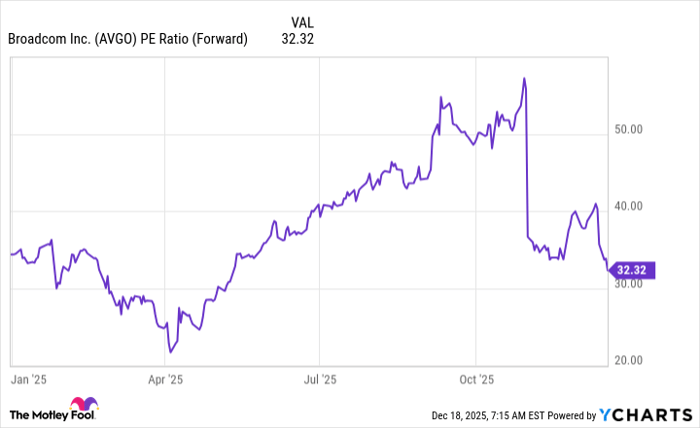

Following the sell-off, Broadcom’s stock now trades for about 32 times expected forward earnings.

AVGO PE Ratio (Forward) data by YCharts.

Considering the monster AI-related growth the company expects over the next few years, I think this is a great price to pay for Broadcom’s stock. Its AI semiconductor revenue will continue to rise throughout 2026, which will eventually get the market excited about the stock again. But until it does, the stock looks like a great value.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $509,039!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,109,506!*

Now, it’s worth noting Stock Advisor’s total average return is 972% — a market-crushing outperformance compared to 193% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of December 22, 2025.

Keithen Drury has positions in Amazon, Broadcom, and Nvidia. The Motley Fool has positions in and recommends Amazon and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.