The artificial intelligence (AI) revolution has transformed NVIDIA Corporation NVDA into one of the most closely watched stocks on Wall Street. The company has emerged as the dominant supplier of graphics processing units (GPUs) that power AI training and inference workloads across data centers, cloud platforms and enterprise applications. Over the past two years, NVIDIA’s explosive growth has helped it become one of the largest companies in the world ($5.05 trillion in market capitalization) and a key beneficiary of the AI spending boom.

Despite its leadership position, NVIDIA stock has delivered relatively modest gains this year. Shares have rallied 11.9% year to date, lagging the broader Zacks Computer and Technology sector’s 16.2% rise.

The stock has also significantly underperformed several semiconductor peers, including Marvell Technology, Inc. MRVL, Intel Corporation INTC and Advanced Micro Devices, Inc. AMD. Year to date, shares of Marvell Technology, Intel and Advanced Micro Devices have surged 239.9%, 198.9% and 129%, respectively.

NVIDIA YTD Price Return Performance

Image Source: Zacks Investment Research

Such underperformance has raised an important question for investors: Is it time to exit the investment, or does NVIDIA still have meaningful upside ahead?

The answer largely depends on whether the company can sustain its AI-driven momentum. While competitors are making progress in AI chips, NVIDIA continues to enjoy a substantial lead in hardware, software and ecosystem development. Its CUDA platform remains the industry standard for AI developers, creating a powerful competitive moat that is difficult for rivals to replicate.

At the same time, investors should recognize that NVIDIA is no longer an early-stage AI story. Recent business trends suggest that the AI spending cycle is far from over, boosting NVIDIA’s prospects.

AI Demand Remains a Powerful Growth Driver for NVIDIA

NVIDIA continues to benefit from unprecedented demand for AI infrastructure. Major cloud providers, enterprises and governments are investing billions of dollars in AI computing capacity, and NVIDIA remains the preferred supplier for many of these projects.

The company’s latest GPU platforms, including its Blackwell architecture, are seeing strong adoption as customers seek higher performance and greater energy efficiency. Large technology companies continue to expand their AI data center footprints, creating a long runway for NVIDIA’s products.

In the first quarter of fiscal 2027, the data center end market generated $75.25 billion in revenues, representing 92% of total sales. This marked a staggering 92% year-over-year increase and 21% sequential growth. The robust growth was driven by the ramp-up of Blackwell 300 products and demand for InfiniBand, Spectrum-X Ethernet and NVLink solutions.

Beyond hardware, NVIDIA has successfully built a software ecosystem that strengthens customer loyalty. Its AI software tools, networking products and enterprise solutions allow the company to capture additional revenue streams while making it more difficult for customers to switch to competing platforms.

As AI applications expand from model training to inference and real-world deployment, NVIDIA is positioned to benefit from multiple phases of the AI growth cycle.

NVIDIA’s Resilient Financial Performance

Despite ongoing macroeconomic challenges, geopolitical issues, and trade and tariff wars, NVIDIA’s financials remain rock solid. In the first quarter of fiscal 2027, revenues jumped 85% year over year to $81.62 billion, while non-GAAP earnings per share rose 140% to $1.87.

NVIDIA’s outlook for the second quarter of fiscal 2027 remains upbeat. The company expects second-quarter revenues to increase approximately 95% year over year to $91 billion, reflecting continued momentum in AI-driven demand. The non-GAAP gross margin is expected to be strong at 75%, indicating a 230-basis-point improvement from the year-ago quarter’s 72.7%.

The Zacks Consensus Estimate for fiscal 2027 and 2028 suggests continued growth momentum for the company’s top and bottom lines.

Image Source: Zacks Investment Research

NVIDIA’s cash flow generation also remains robust. During the first quarter of fiscal 2027, NVIDIA generated $50.3 billion in operating cash flow and $48.6 billion in free cash flow. The company ended the first quarter with $80.6 billion in cash, cash equivalents and marketable securities, up from $62.6 billion in the previous quarter.

This strong liquidity position enables NVIDIA to reinvest in research and development, expand manufacturing capabilities and return capital to shareholders. In the first quarter, the company returned $243 million to its shareholders through dividend payouts and repurchased stocks worth $19.3 billion.

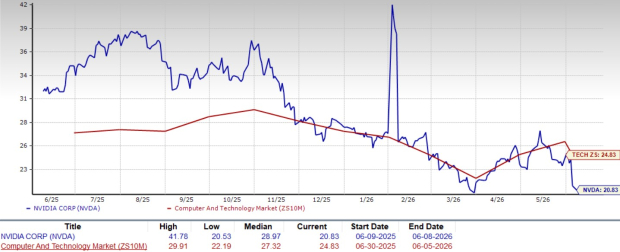

Valuation Suggests NVDA Stock Is Not Overpriced

Although NVIDIA remains one of the market’s most valuable companies, its valuation appears reasonable relative to growth prospects.

The stock currently trades at a forward 12-month price-to-earnings (P/E) multiple of 20.83. This is below the semiconductor industry average of 24.83.

NVIDIA Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

NVIDIA’s valuation is also significantly lower than that of semiconductor peers such as Advanced Micro Devices, Marvell Technology and Intel. At present, Advanced Micro Devices, Marvell Technology and Intel trade at forward 12-month multiples of 53.03, 60.90 and 90.29, respectively.

A lower valuation multiple is notable because NVIDIA arguably possesses stronger growth prospects, higher profitability and a more dominant competitive position than many of its rivals. This suggests that investors are not paying an excessive premium for the company’s future earnings potential.

If NVIDIA continues delivering strong financial results, the current valuation could leave room for additional upside over the long term.

Conclusion: Hold NVDA Stock Tightly

While NVIDIA’s 11.9% year-to-date gain may look disappointing compared with several semiconductor peers, the stock’s underperformance does not necessarily signal weakening fundamentals. In many cases, rival stocks have benefited from recovery stories, while NVIDIA has already been operating from a position of strength.

The company remains the clear leader in AI infrastructure, continues to benefit from massive industry spending trends and trades at a valuation below both the industry average and several major competitors. These factors support a favorable long-term investment outlook.

For investors with a multi-year time horizon, holding NVIDIA appears to be the more compelling strategy. Although short-term volatility is always possible, the company’s leadership in AI, strong financial performance and attractive valuation suggest that its growth story is far from over.

NVIDIA currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

Intel Corporation (INTC) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Marvell Technology, Inc. (MRVL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.