Key Points

-

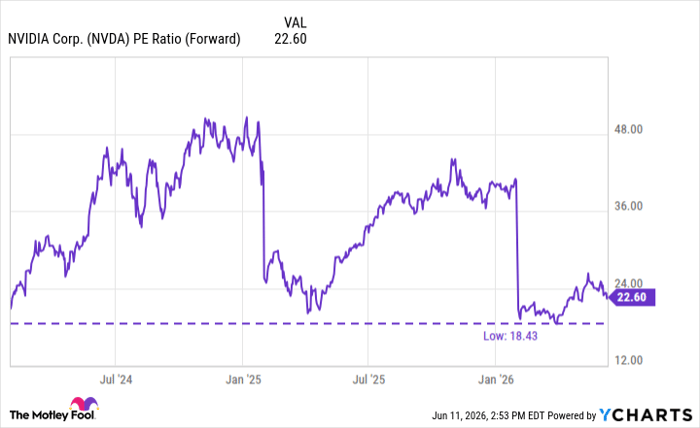

Nvidia currently trades at a forward P/E ratio of 22.

-

Throughout 2026, Nvidia’s forward earnings multiples have traded in a tight range between 18 and 25.

-

Nvidia’s forward P/E has not traded in this range since before the artificial intelligence (AI) revolution.

- 10 stocks we like better than Nvidia ›

So far this year, Nvidia (NASDAQ: NVDA) stock has gained 8% — placing it slightly above the returns in the S&P 500 and nominally trailing those seen in the Nasdaq.

From a valuation perspective, the world’s most valuable company boasts a forward price-to-earnings (P/E) ratio of about 22. Moreover, Nvidia’s forward P/E has spent much of 2026 locked in a narrow corridor between roughly 18 and 25.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

This steadiness raises two questions: When was the last time investors saw Nvidia’s forward multiple behave this way and what happened next?

Image source: Nvidia.

Nvidia’s valuation profile echoes its pre-AI boom

Per the chart below, investors can see that Nvidia’s forward P/E has not traded inside a comparable, compressed band since before the artificial intelligence (AI) revolution. Prior to the outburst of generative AI models back in late 2022, the market largely viewed Nvidia as a company primarily focused on graphics and gaming with a data center services side hustle.

NVDA PE Ratio (Forward) data by YCharts.

Once ChatGPT, Anthropic’s Claude, and a handful of other frontier models arrived, demand for accelerated computing exploded. As it turns out, Nvidia’s first-mover advantage in designing graphics processing units (GPUs) was uniquely positioned for this moment. Hence, the company’s revenue and earnings rose dramatically virtually overnight. Subsequently, Nvidia’s forward earnings valuation multiple broke out and spent the next few years oscillating at levels frequently above 40.

The current range represents a reversion to a pre-AI boom rhythm. Against this backdrop, the current sideways trading seen in Nvidia is the first real extended stretch of valuation stability since the world began pricing the company as the indispensable king of AI infrastructure build-outs.

Don’t let valuation distract you from Nvidia’s guidance

Nvidia’s valuation profile looks even more striking when set against the company’s actual operating momentum. During the fiscal 2027 first quarter (ended April 26,2026), revenue from Nvidia’s data center segment surged 92% year over year, reaching $75 billion. Management forecasted total revenue to be $91 billion next quarter, plus or minus 2%. This represents an acceleration quarter over quarter and a staggering 95% year-over-year growth.

To me, a forward earnings multiple stuck around 22 does not necessarily signal skepticism about Nvidia’s near-term earnings power. Instead, I think it reflects a situation whereby the market has already baked in meaningful growth and is no longer willing to pay the premium multiples witnessed throughout 2023 to 2025.

In other words, range-bound valuation multiples can be normal when investors simply expect continued strong top- and bottom-line expansion. These dynamics are actually quite common for mature, high-growth technology platforms.

Nvidia is positioned for another leg of valuation expansion

After Nvidia’s forward P/E dropped sharply to about 18 earlier this year, the multiple has more recently stabilized and begun to edge modestly higher within a tight range. This could suggest that early stages of valuation expansion are in the works. Perhaps the clearest reason why is Nvidia’s growing number of strategic partnerships. These are the clearest catalysts for Nvidia’s next leg up.

The company has invested billions of dollars in Nokia, Coherent, Lumentum, and Marvell Technology to fortify high-speed optical interconnects and advanced networking. These technologies are becoming increasingly important as hyperscalers allocate capital expenditure (capex) beyond GPU procurement and build more sophisticated infrastructure stacks within AI factories. Moreover, these relationships unlock numerous opportunities for Nvidia beyond data centers — opening the door to scalable edge computing, robotics platforms, and autonomous vehicle systems.

These moves quietly broaden Nvidia’s total addressable market (TAM) beyond chips. I think the company has started laying the groundwork to justify higher valuation multiples once execution catches up with these new opportunities. History suggests that if Nvidia’s strong guidance is delivered, the current range-bound phase should turn out to be nothing more than a temporary consolidation before the next chapter of significant valuation rerating unfolds.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $433,268!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,259,391!*

Now, it’s worth noting Stock Advisor’s total average return is 935% — a market-crushing outperformance compared to 206% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of June 13, 2026.

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Coherent, Lumentum, Marvell Technology, and Nvidia. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.