Medpace Holdings, Inc. MEDP offers a focused view of how clinical research organization demand is changing in 2026.

The company’s growth story is not just about trial volume. It also turns on which therapeutic areas are holding up, how quickly awards convert to revenues, and whether technology spending can improve productivity later.

Medpace Shows a Split in Trial Demand

Demand across Medpace’s book is becoming more uneven by therapeutic area. Metabolic and GLP-1 programs have historically carried lower cancellation rates, giving that work a stabilizing role in backlog quality and utilization.

Oncology and cardiovascular have been the larger sources of recent cancellations. That matters because both remain important pieces of Medpace’s clinical-development base, and pressure in those areas can weigh on forward visibility even when other categories remain steadier.

The same theme is relevant across the broader clinical services group. IQVIA Holdings Inc. IQV, which provides clinical research services, healthcare intelligence and technology solutions, is another name investors often watch when trial starts and sponsor spending patterns shift.

MEDP Awards Point to a Longer Conversion Cycle

Medpace’s early award signals are not translating into immediate revenues. Initial award notifications and win rates have improved, but many awards remain in pre-backlog before moving into active projects.

The timing gap is meaningful. Awards can take three to five quarters to start, which means improved pipeline activity may support later-period growth rather than near-term acceleration.

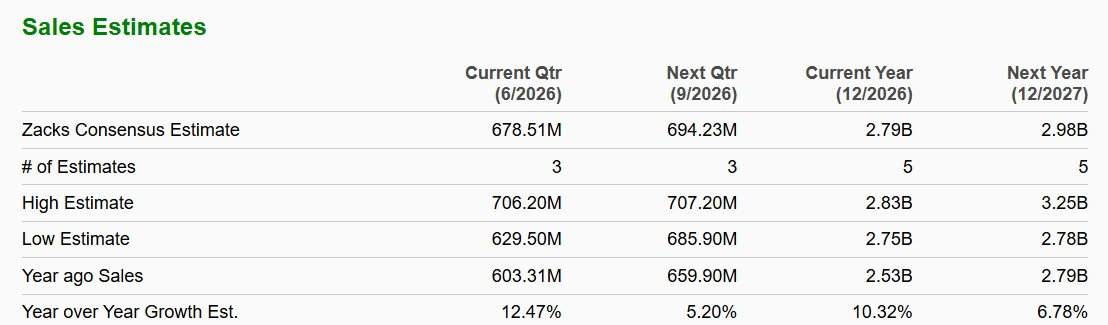

That delayed conversion cycle helps explain why backlog can support continuity without proving a sharp rebound. Medpace expects roughly $1.9 billion to $1.94 billion of backlog to convert into revenues over the next 12 months, but first-quarter net book-to-bill was 0.88X.

Image Source: Zacks Investment Research

Medpace Margins Benefit From Full-Service Focus

Medpace’s full-service model has helped protect profitability through mix changes. First-quarter EBITDA was $149.4 million, and EBITDA margin was 21.1%, nearly in line with 21.2% in the year-ago period.

That stability came despite elevated reimbursed out-of-pocket activity. Pass-throughs were roughly 44% of revenues in the quarter, creating mix noise that can make reported growth and booking comparisons harder to read.

Execution is becoming as important as volume. Improved employee retention, operating discipline and a centralized full-service platform give Medpace tools to defend margins while demand patterns normalize.

Charles River Laboratories International, Inc. CRL gives investors another angle on outsourced research demand. Its preclinical and drug-development services sit earlier in the development chain, so its trends can complement what Phase I-IV focused companies reveal about clinical activity.

MEDP AI Spending Raises a Near-Term Question

Medpace’s technology investment adds another layer to the 2026 growth debate. Artificial intelligence spending is expected to exceed savings through 2026-2027, limiting the near-term productivity benefit.

That does not make the spending unimportant. It shows how healthcare-services companies may need to absorb upfront technology costs before automation, analytics or workflow improvements show up in margins.

For investors, the question is timing. AI can support better execution over time, but the current setup points to expense absorption before measurable operating leverage.

Medpace Scores Reflect Growth With Restraint

The bottom line is that Medpace sits in a healthier position than its softer booking signals suggest, but the trend picture still requires patience. Backlog conversion, metabolic exposure and durable margins support the story, while cancellations, longer start times and AI spending keep the near-term setup measured.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #3 (Hold). That indicates a more balanced short-term earnings-revision profile rather than a clear positive or negative signal. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Medpace’s Style Scores sharpen that view. Its Growth Score of A points to attractive growth characteristics, while its Momentum Score of C is more neutral and its Value Score of D signals less obvious valuation support. The VGM Score of B suggests the broader style profile remains constructive, but not enough by itself to override the more restrained Zacks Rank #3 signal.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Medpace Holdings, Inc. (MEDP) : Free Stock Analysis Report

Charles River Laboratories International, Inc. (CRL) : Free Stock Analysis Report

IQVIA Holdings Inc. (IQV) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.