Uranium Energy Corp. UEC is increasingly tied to a broader U.S. nuclear fuel and critical-minerals story. The company has moved beyond a simple uranium price trade by pairing domestic in-situ recovery production with a proposed conversion platform.

That strategy gives UEC a place in supply-security discussions. Investors still need to separate the long-term theme from near-term execution.

How UEC Fits the U.S. Fuel Security Push

UEC holds what it describes as the largest uranium resource base and most licensed production capacity in the United States. Its Wyoming and South Texas hub-and-spoke in-situ recovery operations total about 12 million pounds of licensed annual capacity.

The operating model matters because multiple mines can feed central processing infrastructure. Christensen Ranch is processed through the Irigaray Central Processing Plant, while Burke Hollow and Palangana feed the Hobson Processing Facility.

Cameco Corporation CCJ provides a useful industry reference point because it is a large uranium and nuclear fuel supplier with exposure across the global fuel cycle. That makes Cameco a benchmark for assessing how far UEC must still go to turn domestic resources into durable fuel-cycle earnings.

Why Uranium Energy Is Chasing Conversion Capacity

UEC’s next strategic layer is United States Uranium Refining & Conversion Corp., or UR&C. The subsidiary is pursuing a new uranium refining and conversion facility in the United States, which would move the company beyond mining and yellowcake production.

UR&C has received a U.S. Nuclear Regulatory Commission docket number for the planned conversion facility. Engineering and design work with Fluor is continuing, and the formal license application is expected after design work is completed and a site is selected.

Management views Western conversion capacity as an acute bottleneck. Centrus Energy Corp. LEU, which is focused on nuclear fuel and high-assay low-enriched uranium, shows why investors are watching fuel-cycle infrastructure beyond mining.

UEC Growth Trend Depends on Permits and Timing

Policy support does not eliminate the need for approvals, construction and wellfield performance. At Christensen Ranch, three new header houses in Wellfield 11 began production late in the third quarter of fiscal 2026 after state approval, while one more was complete and awaiting approval.

Sweetwater reinforces the same point. The Wyoming project has FAST-41 transparency status, and the Bureau of Land Management completed its completeness review of UEC’s Plan of Operations for in-situ recovery operations.

Those milestones are useful, but timing remains central to the investment case. Site selection, licensing and construction will determine when strategic projects can shift from policy-aligned assets to economic contributors.

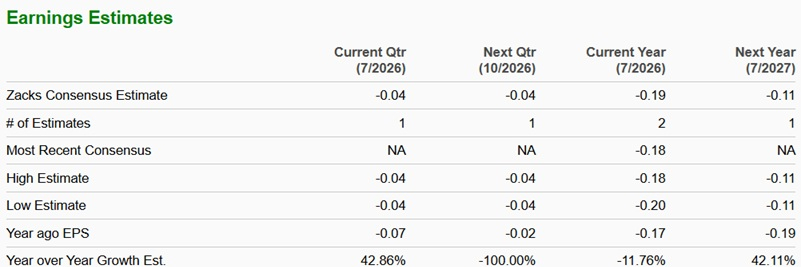

The Zacks Consensus Estimate for UEC for fiscal 2026 is currently pegged at a loss of 19 cents per share, wider than the loss of 17 cents reported in fiscal 2025. The consensus for fiscal 2027 also suggests a loss of 11 cents per share, as shown in the chart below.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

How Uranium Energy Adds Critical Mineral Exposure

UEC’s Alto Paraná project in Paraguay gives the company an adjacent critical-minerals angle through titanium and vanadium. An independent report concluded that the project could contribute to the security and diversification of U.S. supply chains.

The preliminary economic assessment included two development cases. The first showed an net present value (NPV) of $419 million and a 21% post-tax internal rate of return, while the larger-scale case showed an NPV of $1.55 billion and a 25% post-tax internal rate of return.

That optionality broadens UEC’s strategic narrative. It does not replace the core uranium thesis, but it gives investors another asset tied to supply-chain diversification.

What UEC’s Ratings Say About This Trend Trade

The bottom line is that UEC’s thematic reach is expanding faster than its near-term stock signal. The company has licensed U.S. capacity, a conversion initiative and critical-mineral exposure, but investors still need proof that execution can become steadier.

UEC currently carries a Zacks Rank #4 (Sell). That short-term rating points to caution over the next one to three months, particularly while the company is still working through production variability, cost pressure and licensing milestones.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Style Scores reinforce that view. UEC has a VGM Score of F, Value Score of F, Growth Score of F and Momentum Score of D. Since higher Style Scores are generally more favorable, these weak grades suggest a less attractive setup across valuation, growth and price-action factors.

For now, the U.S. nuclear fuel and critical-minerals theme gives UEC a clearer strategic identity. The stock still needs cleaner execution, better momentum and more durable earnings support before that theme translates into a stronger signal.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Uranium Energy Corp. (UEC) : Free Stock Analysis Report

Cameco Corporation (CCJ) : Free Stock Analysis Report

Centrus Energy Corp. (LEU) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.