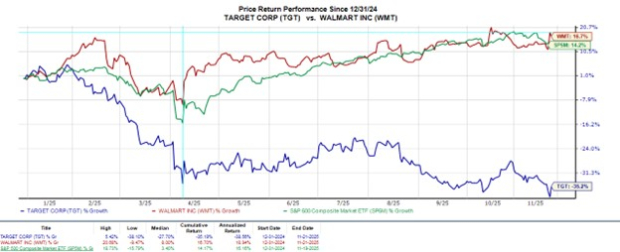

Target TGT and Walmart WMT offered insight into the strength of the consumer in their Q3 reports this week, and both were able to pleasantly beat earnings expectations.

This has made the conversation more riveting as to whether it’s time to buy stock in either of these omnichannel retail giants. To that point, investors have been eying Walmart stock for more upside and Target shares for a rebound, along with its more enticing dividend and cheaper valuation.

However, thanks to a tech-driven shift from a traditional retailer to having a massive online presence, Walmart’s growth has been captivating. Showing signs of a turnaround, Target has tried to follow suit in a bid to offset its exposure to more discretionary items that have coincided with weaker store traffic.

Image Source: Zacks Investment Research

Target & Walmart Q3 Review

Despite choppy consumer discretionary spending, Target’s Q3 EPS of $1.78 beat expectations of $1.76 per share although this was down from $1.85 in the prior year quarter. Attributed to what it called affordability pressures on consumer goods, Target’s Q3 sales dipped over 1% year over year to $25.27 billion and slightly missed estimates of $25.35 billion.

Meanwhile, Walmart’s global e-commerce expansion led to its Q3 sales rising 6% YoY to $179.49 billion, topping estimates of $177.14 billion by 1%. Walmart’s Q3 EPS of $0.62 edged estimates of $0.61 and was up from $0.58 per share a year ago.

Guidance & Outlook

Signaling confidence heading into the holiday shopping season, Walmart now expects its current fiscal 2026 net sales growth at 4.8%-5.1%, up from its prior guidance range of 3.75%-4.75%. Additionally, Walmart raised its guidance for full-year operating income by nearly 400 basis points to a growth range of 8.5%-9.5%.

As for Target, the retailer cut the top end of its full-year profit outlook, guiding its current FY26 EPS at $7.00-$8.00 from previous expectations of $7.00-$9.00. Taking a more cautious stance on the holiday outlook, Target did not provide revenue guidance, with the retailer highlighting ongoing softness in discretionary categories but strength in food, beverage, and digital sales.

Following the Trend of EPS Revisions

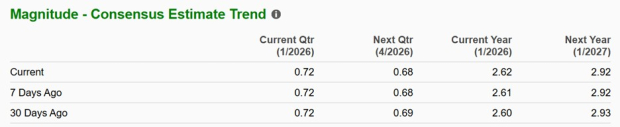

While Target’s updated FY26 EPS guidance still falls in range of the Zacks Consensus of $7.30, it’s noteworthy that this would be a 17% drop from $8.86 per share in its FY25. That said, FY27 EPS is projected to stabilize and rise 9% to $7.94.

Taking away from the anticipated rebound in Target’s bottom line is that FY27 EPS estimates are down 6% in the last month, and FY26 EPS estimates have dipped more than 1%.

Image Source: Zacks Investment Research

Pivoting to Walmart, annual earnings are now expected to rise 4% in FY26 and are projected to jump another 12% in FY27 to $2.92 per share. In the last 30 days, Walmart’s FY26 EPS estimates are modestly higher, but FY27 EPS estimates are slightly down.

Image Source: Zacks Investment Research

Bottom Line

Following their Q3 reports, Target and Walmart stock have retained a Zacks Rank #3 (Hold) as a more compelling trend of EPS revisions has been needed to suggest more upside in WMT or a rebound in TGT. Considering such, Walmart’s EPS beat and optimistic outlook could get the needle going in this regard, while Target’s cautious stance could dim its prospects.

Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).