Datadog DDOG delivered strong fourth-quarter 2024 results that exceeded the Zacks Consensus Estimate, but shares tumbled approximately 9% as the company’s conservative 2025 guidance overshadowed the impressive performance. Investors now face a critical decision: hold their positions or wait for a better entry point in what appears to be a transitional year for the cloud monitoring leader.

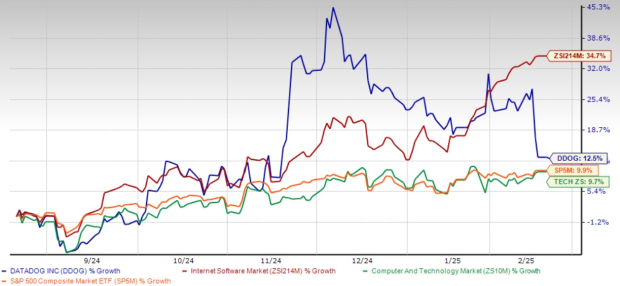

Datadog has emerged as a formidable leader in the cloud monitoring and security space, with its stock rising 12.5% over the past six months. Despite operating in a competitive landscape with established players like New Relic, Dynatrace and Splunk, DDOG has successfully differentiated itself through its unified platform approach and comprehensive multi-cloud integrations.

6-Month DDOG Stock Price Performance

Image Source: Zacks Investment Research

At the heart of Datadog’s strategy is its ability to provide comprehensive visibility across multi-cloud infrastructures. By integrating deeply with Amazon AMZN-owned Amazon Web Services, Alphabet GOOGL-owned Google Cloud and Microsoft MSFT Azure, Datadog enables organizations to monitor, analyze and optimize their entire cloud ecosystem from a single platform. This unified approach is particularly valuable as businesses increasingly adopt hybrid and multi-cloud strategies to enhance flexibility and avoid vendor lock-in.

DDOG Crushes Q4 Results

The cloud observability platform reported robust fourth-quarter 2024 results with revenue reaching $738 million, up 25.1% year over year and comfortably exceeding analyst expectations of $714 million. Non-GAAP earnings per share came in at 49 cents, which surpassed the consensus mark of 43 cents and increased 11.4% from the year-ago quarter.

Datadog’s customer metrics remained strong, with the company reporting approximately 30,000 customers by the quarter’s end, up from 27,300 a year ago. More importantly, customers generating annual recurring revenue (ARR) of $1 million or more increased to 462, up 17% year over year, while customers with ARR of $100,000 or more grew 13% to about 3,610.

The company’s platform strategy continues to resonate with customers. By the end of the fourth quarter, 83% of customers were using two or more products, 50% were using four or more (up from 47% a year ago), and 26% were using six or more (up from 22%). These cross-selling metrics indicate Datadog’s success in expanding within its existing customer base.

Datadog’s Concerning 2025 Outlook

Despite the strong fourth-quarter results, Datadog’s guidance for fiscal 2025 disappointed investors. The company projected revenues between $3.175 billion and $3.195 billion, suggesting 18-19% growth, substantially below the 25% growth achieved in fourth-quarter 2024. First-quarter 2025 revenue guidance of $737-$741 million implies just 21% year-over-year growth and minimal sequential growth from the fourth quarter.

The decelerating growth trajectory caught investors off guard, especially considering the company’s record bookings quarter with more than $1 billion in bookings for the first time. Management attributed the conservative outlook to their guidance philosophy, which bases projections on recent trends with added conservatism rather than incorporating potential acceleration from increased investments.

The Zacks Consensus Estimate for 2025 revenues is pegged at $3.19 billion, indicating 18.79% growth year over year. The consensus mark for earnings has moved south by a penny to $1.93 per share over the past 30 days. The figure indicates growth of 6.04% year over year.

Image Source: Zacks Investment Research

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

AI Impact and Growth Investments

Datadog’s AI-related business continues to show promise, with AI native customers representing approximately 6% of fourth-quarter ARR and contributing about five percentage points to year-over-year revenue growth. The company noted that while the adoption of AI workloads brings opportunities, the immediate monetization of GPU monitoring remains limited as these workloads are still primarily confined to AI native companies rather than mainstream enterprise adoption.

Management remains bullish on long-term prospects, emphasizing its commitment to investing for future growth. The company plans to grow operating expenses in the high 20% range year over year in 2025, with significant investments in both sales and marketing and R&D. This spending strategy aims to capitalize on opportunities in under-penetrated geographies, channel partnerships and enterprise accounts.

Strategic Product Developments of DDOG

The company highlighted several strategic product developments, including the general availability launch of Datadog On-Call and strong customer interest in their flex logs solution. Management noted a competitive opening in the log management space due to recent M&A activity among competitors, which could present growth opportunities.

Datadog also expanded its security offerings, launching a modern approach to Cloud SIEM that doesn’t require dedicated staff, and enhanced its Kubernetes monitoring capabilities. These developments strengthen the company’s competitive position in observability and adjacent markets.

Investment Perspective: Hold DDOG or Wait?

For current shareholders, maintaining positions may be prudent despite near-term volatility. Datadog’s strong platform adoption metrics, expanding product portfolio, and investments in growth initiatives suggest the company is positioning for long-term success. The 29% free cash flow margin demonstrates financial strength that supports these investments while maintaining profitability.

However, new investors might benefit from waiting for a better entry point. The significant disconnect between record bookings and conservative revenue guidance suggests a transitional period as Datadog digests recent customer optimizations and investments take time to yield results. Management explicitly noted that sales and marketing investments typically impact results in one to two years, while R&D investments show returns in two to three years.

The stock’s valuation remains pricey despite the post-earnings pullback, reflecting Datadog’s market leadership but offering a limited margin of safety if growth continues to decelerate. The stock trades at a premium with a forward 12-month P/S ratio of 13.54x compared to the broader Zacks Internet – Software industry’s 3.15x.

DDOG P/S Ratio Depicts Stretched Valuation

Image Source: Zacks Investment Research

Potential investors should monitor enterprise AI adoption trends, which could accelerate Datadog’s growth beyond conservative projections if mainstream companies begin deploying more AI workloads.

Conclusion

In conclusion, while Datadog’s fourth-quarter results demonstrate continued execution excellence, the tempered 2025 outlook warrants caution. Long-term investors should hold positions through this transitional period, while those looking to establish new positions might benefit from patience as the company’s investments mature and growth potentially reaccelerates in late 2025 or 2026. DDOG stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Datadog, Inc. (DDOG) : Free Stock Analysis Report