ImmuCell Corporation ICCC has received a recommendation upgrade to “Outperform,” driven by consistent execution across its sales and gross margin profile, alongside emerging strategic optionality linked to its late-stage mastitis treatment, Re-Tain. The company’s operational rebound, product mix strength and capacity scaling provide a solid base for continued performance, while developments in product innovation and regulatory progress introduce asymmetric upside potential.

Price Performance

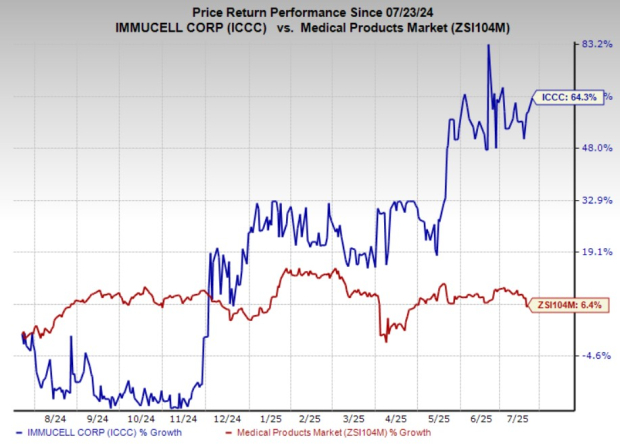

ICCC shares have outperformed the industry in the past year. The stock has surged 64.3% against the industry’s 6.4% growth in the said period.

Image Source: Zacks Investment Research

Sales Execution & Market Penetration

ImmuCell posted a record $8.1 million in product sales for the first quarter of 2025, an 11% year-over-year increase, signaling robust demand across its First Defense line. The expansion of production capacity to support more than $30 million in annual sales has enabled the company to reduce its order backlog from $4.4 million at the end of 2024 to $3.4 million by early May 2025, clearing the way for salesforce mobilization and uninterrupted customer fulfillment.

The Tri-Shield formulation — offering combined protection against E. coli, coronavirus and rotavirus — accounted for approximately 71% of the product mix in the quarter, reflecting strong customer preference for broader-spectrum coverage. This positions the company as a competitive alternative to traditional dam-level vaccines, especially as distribution channels broaden through enhanced direct-to-end-user engagement and regional sales management coverage.

Gross Margin Recovery & Operating Leverage

The gross margin improved sharply to 42% in the first quarter of 2025 from 32% in the prior-year period and 37% in the fourth quarter of 2024. This recovery reflects enhanced yields, reduced contamination-related scrap, and fixed-cost leverage across an expanded manufacturing footprint.

Adjusted EBITDA rose to $2.3 million in the first quarter of 2025 from $0.46 million a year earlier. Over the trailing 12 months, adjusted EBITDA stood at $3.3 million, a significant rebound from a $280,000 loss in the prior year.

This margin and cash generation trajectory is further bolstered by improved liquidity — $4.6 million in cash, $12.1 million in working capital and a fully undrawn $1-million credit line as of March 2025. The company also maintains a strong equity base with $29 million in stockholders’ equity.

Product Innovation & New Format Launch

A critical driver of near- to mid-term expansion is the second-half 2025 launch of a bulk powder version of First Defense. Unlike the existing capsule and gel formats, the powder formulation targets calf ranches with feed-based administration preferences, representing a previously underpenetrated market segment. Though it is not USDA-claimed, early customer interest and the format’s scalability support the company’s “Beyond Vaccination” positioning.

This initiative is expected to broaden ImmuCell’s market access and enhance unit economics while diversifying revenue streams away from its current format-constrained sales model.

Optionality Through Re-Tain & FDA Review

While not yet contributing to revenues, Re-Tain — a novel, non-antibiotic treatment for subclinical mastitis — represents an embedded strategic option. As of early 2025, the product remains under FDA New Animal Drug Application review, following four Chemistry, Manufacturing, and Controls submissions. The company has initiated investigational product use in the field during the second half of 2025 to gather real-world performance feedback.

Although regulatory delays and the expiration of key Drug Product contract manufacturing agreements introduce risks, a Controlled Launch strategy has been outlined. This plan restricts initial commercialization to selected farms, prioritizing data collection and quality assurance.

Outlook

In summary, the OUTPERFORM rating reflects ImmuCell’s demonstrated ability to scale sales and margin through the execution of its core First Defense franchise, the strategic expansion into new formats aimed at untapped markets, and the embedded upside in Re-Tain’s potential FDA approval and commercialization. While risks remain tied to distribution concentration and supply-chain dependencies, the company’s financial stability, operational control and product momentum provide a favorable setup for continued performance.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

ImmuCell Corporation (ICCC) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).