Boot Barn Holdings, Inc. BOOT gives investors a clear trade-off. Sales trends, store growth and digital momentum remain healthy, but the margin outlook is less clean.

The stock is not an obvious bargain. BOOT may still fit growth-oriented investors, but the near-term setup supports patience more than aggressive buying.

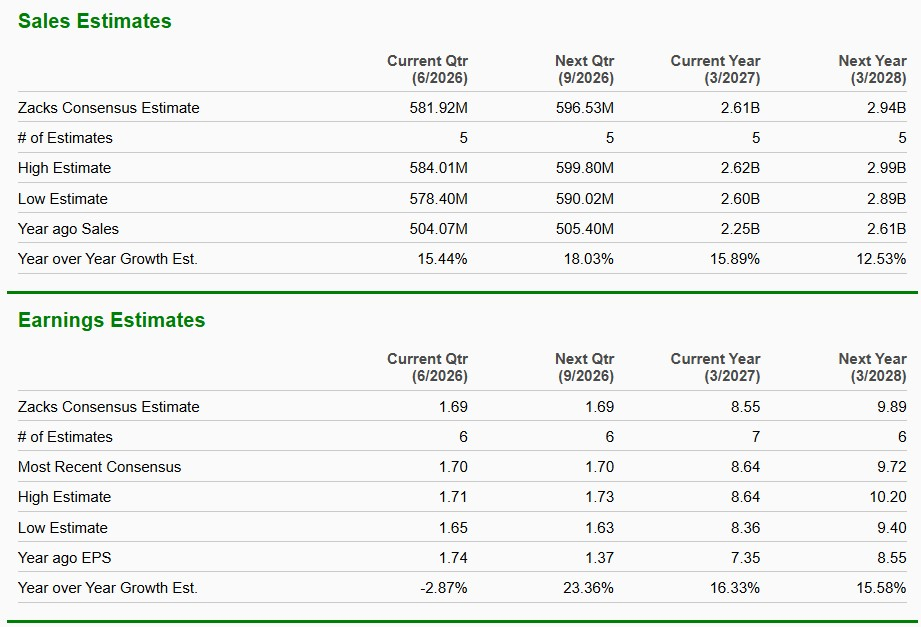

BOOT Sales Growth Looks Hard to Ignore

BOOT expects fiscal 2027 net sales to grow 14% to 16% year over year, supported by 70 planned store openings and continued same-store sales gains. Management projects consolidated same-store sales growth of 2% to 4%, with retail stores up 1% to 3%.

E-commerce remains the faster-growing channel, with same-store sales expected to rise 11% to 13% for fiscal 2027. Recent results support that outlook. Fourth-quarter fiscal 2026 net sales rose 18.7% to $538.8 million, while consolidated same-store sales increased 6.1%.

New-store economics add to the bullish case. Boot Barn targets about $3.2 million in first-year sales per new store, with roughly $1.7 million of total net investment and a payback period of about 1.8 years.

Boot Barn Holdings, Inc. Price, Consensus and EPS Surprise

Boot Barn Holdings, Inc. price-consensus-eps-surprise-chart | Boot Barn Holdings, Inc. Quote

Boot Barn Margins Face a Tough Near-Term Test

Margin pressure is the key reason to avoid chasing the stock. For the first quarter of fiscal 2027, Boot Barn expects gross margin of 37.1% to 37.3%, down from 39.1% in the year-ago period.

The full-year picture is also softer. Fiscal 2027 gross margin is expected to be 37.7% to 37.9%, below fiscal 2026’s 38.1%. Higher occupancy, freight and distribution costs are weighing on profitability.

The hurdle rate has also moved higher. Boot Barn expects to leverage buying, occupancy and distribution center costs only at 10% same-store sales growth for fiscal 2027. That means even healthy sales growth may not quickly translate into stronger margins.

BOOT Valuation Looks Balanced, Not Cheap

BOOT trades at 17.54X forward 12-month earnings. That is below the Zacks sector and the S&P 500, but above the Zacks sub-industry multiple of 14.08X.

The stock also sits close to its own five-year median of 18.42X. That makes the valuation look balanced rather than deeply discounted.

A $166 price target, based on 18.59X forward 12-month earnings, leaves some room for upside from the recent stock price. Still, the setup does not scream cheap given the margin risks.

Image Source: Zacks Investment Research

Boot Barn Balance Sheet Supports Patience

Boot Barn has the financial flexibility to keep investing through the margin squeeze. The company ended fiscal 2026 with $141 million in cash and no borrowings under its $250 million revolving credit facility.

Operating cash flow also improved sharply. Net cash provided by operating activities was $304.9 million in fiscal 2026, compared with $147.5 million in fiscal 2025.

The company continues to fund growth, with fiscal 2027 capital expenditures expected at $125-$130 million. It also repurchased 286,504 shares for $50 million during fiscal 2026.

For investors comparing specialty retail names, Academy Sports and Outdoors, Inc. ASO offers another way to assess discretionary spending trends across footwear, apparel and outdoor categories. Tractor Supply Company TSCO is also relevant because rural lifestyle and work-oriented retail demand can overlap with parts of Boot Barn’s customer base.

BOOT Ratings Show Why the Call Is Mixed

The bottom line is that BOOT looks more like a watch-and-selectively-buy growth story than a clear value play. The sales engine is working, but near-term earnings quality is being tested by freight, occupancy and expansion costs.

The stock currently carries a Zacks Rank #3 (Hold). That rank points to a neutral short-term setup rather than a strong near-term buying signal. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are more favorable for growth investors. BOOT has a VGM Score of A, a Growth Score of A and a Momentum Score of A, suggesting solid growth and price-trend characteristics. Its Value Score of C is the offset, reinforcing the view that the stock is better suited to investors prioritizing growth and momentum over a discounted entry point.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report

Tractor Supply Company (TSCO) : Free Stock Analysis Report

Academy Sports and Outdoors, Inc. (ASO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.