HealthEquity, Inc. HQY is benefiting from expanding margins, improving operating leverage and technology-driven efficiency initiatives. The company is also investing in security enhancements and automation tools to strengthen customer service and fraud prevention capabilities. However, despite the improving fundamentals, HealthEquity reflects a balanced risk-reward profile.

The key question for investors is whether stronger profitability and higher guidance can outweigh ongoing exposure to custodial yield fluctuations, cybersecurity-related uncertainties and competitive pressures.

HQY’s Strong Fiscal First-Quarter Performance Supports Outlook

HealthEquity delivered adjusted earnings per share of $1.24 in the first quarter of fiscal 2027, surpassing the Zacks Consensus Estimate by 11.7%. Earnings increased 28% year over year, driven by operating leverage and continued business momentum.

Revenues rose 7% year over year to $354.6 million and modestly exceeded expectations. Growth was supported by contributions from service, custodial and interchange revenues, demonstrating broad-based strength across the business.

HQY Margin Expansion Highlights Operating Leverage

Profitability remained a key highlight during the quarter. Gross profit increased 14.3% year over year to $256.3 million, while gross margin expanded 450 basis points to 72.3%.

Although HealthEquity continued to invest in growth and technology initiatives, margin performance remained strong. Sales and marketing expenses increased 3.3% year over year to $26.8 million, technology and development expenses rose 10.3% year over year to $67.8 million, and general and administrative expenses climbed 21.9% year over year to $31.1 million. Even with these investments, operating income increased 23.9%, resulting in a 390-basis-point expansion in operating margin to 29%.

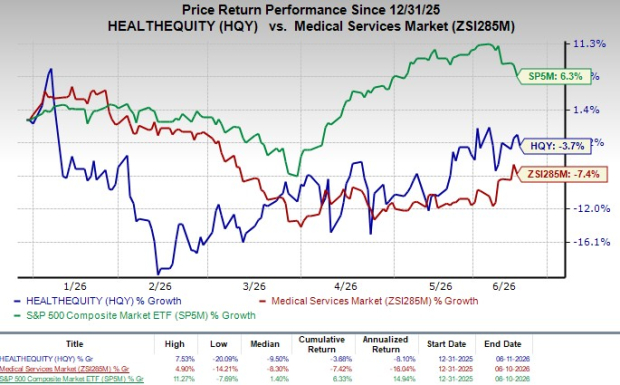

Image Source: Zacks Investment Research

HQY’s Raised Guidance Reflects Confidence

Management raised its fiscal 2027 outlook following the strong start to the year. Revenues are now expected to be in the range of $1.41-$1.42 billion, up from the prior guidance of $1.405-$1.415 billion.

Adjusted earnings per share are now projected to be between $4.66 and $4.73 compared with the earlier range of $4.56-$4.65. The higher outlook reflects stronger participation in enhanced-rate offerings, benefits from the company’s hedging strategy designed to reduce custodial yield volatility and continued operational improvements.

Solid Financial Position Supports Flexibility

HealthEquity ended the quarter with cash and cash equivalents of $265.4 million. Total debt declined to $942.6 million from $957.4 million at fiscal 2026-end, reflecting ongoing balance-sheet improvement.

The company’s interest coverage ratio improved to 6.4 times from 5.9 times at the end of fiscal 2026. Meanwhile, operating cash flow increased significantly to $97.5 million from $64.7 million in the year-ago period, highlighting stronger cash generation and improving earnings quality.

HQY Share Repurchases and Capital Allocation

HealthEquity’s active share repurchase plan is part of the current setup and can support per-share outcomes when operating performance is also improving. Buybacks tend to matter most when they are funded by sustained cash generation and when the business outlook remains stable enough to avoid a reversal in capital priorities.

Risks Remain on the Radar

Despite the favorable operating trends, investors should continue monitoring several risk factors. HealthEquity remains sensitive to changes in custodial yields and client contract dynamics. In addition, cybersecurity-related litigation and regulatory developments continue to create uncertainty.

The company also operates in a competitive environment where larger players such as UnitedHealth Group UNH and Webster Financial WBS possess significant scale and distribution advantages.

Investment Takeaway

HealthEquity is executing well, as evidenced by expanding margins, rising cash flow and increased fiscal 2027 guidance. Management’s focus on automation, fraud reduction and security enhancements is supporting profitability while positioning the business for long-term growth.

However, exposure to custodial yield fluctuations, cybersecurity overhangs and competitive pressures prevents a more aggressive stance at this stage. Consequently, HealthEquity’s current Zacks Rank #3 (Hold) appears appropriate as investors await further confirmation that recent margin gains and guidance improvements can be sustained. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

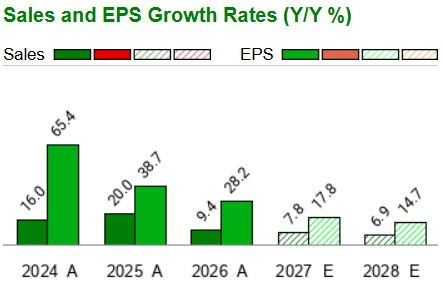

HQY’s Sales & EPS Picture

In fiscal 2027, HQY is expected to experience growth of 7.8% in revenues. On the profitability front, earnings per share are expected to improve 17.8% year over year.

Image Source: Zacks Investment Research

HQY’s Valuation Picture

HQY currently trades at a forward 12-months price-to-sales ratio of 5.2X, above its industry’s current level of 0.5X.

Image Source: Zacks Investment Research

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

UnitedHealth Group Incorporated (UNH) : Free Stock Analysis Report

Webster Financial Corporation (WBS) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.