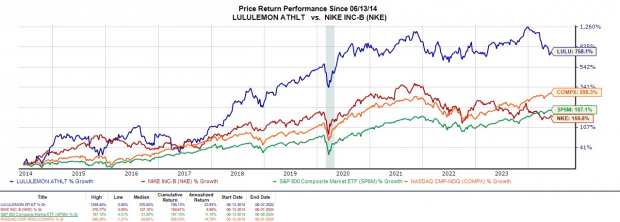

The world of retail is akin to a high-stakes poker game, and companies like Lululemon LULU are constantly raising the ante to entice investors. Despite industry-wide concerns about a downturn in consumer spending, Lululemon surged ahead, outshining expectations in its recent Q1 earnings report. With competitors like Nike NKE feeling the heat, the question now looms – is the time ripe to dive into Lululemon’s stock, especially with a year-to-date plunge of -37%?

Image Source: Zacks Investment Research

Q1 Performance & Future Projections

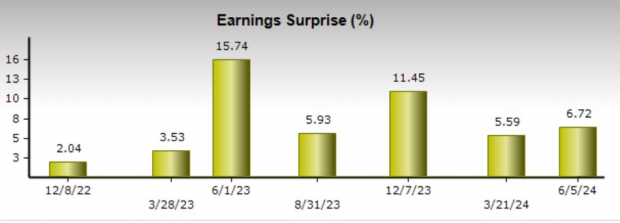

In a deft display of resilience, Lululemon’s Q1 revenue hit $2.2 billion, marking a robust 10% increase from the previous year and slightly surpassing estimates. The cherry on top was the Q1 EPS of $2.54, beating expectations by 7% and showing an impressive 11% surge from a year ago. The icing on the cake? Lululemon has been outperforming earnings forecasts for 16 consecutive quarters spanning back to September 2020.

Image Source: Zacks Investment Research

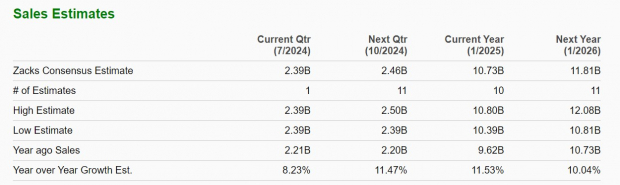

Looking forward to the second quarter, Lululemon anticipates a 9%-10% growth in revenue, slightly eclipsing the current Zacks Consensus forecast of 8.23% or sales totaling $2.39 billion. The company maintains its full-year revenue growth expectations in the 10%-11% range, with analysts projecting a sturdy 11.53% growth for the fiscal year.

Image Source: Zacks Investment Research

Earnings Per Share Performance

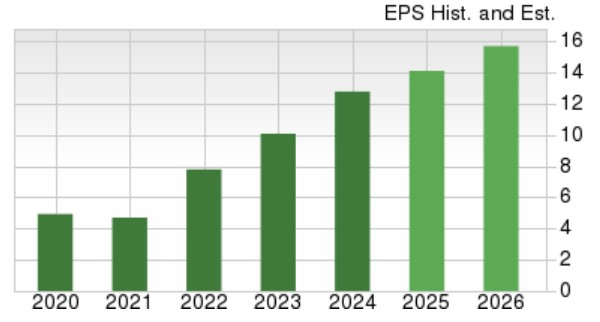

According to Zacks projections, Lululemon’s annual earnings are on a steady ascent, expected to increase by 11% in the current fiscal year 2025, reaching $14.14 per share compared to $12.77 in FY24. Future prospects look even brighter, with a forecasted 11% leap in EPS to $15.68 for FY26.

Image Source: Zacks Investment Research

Key Takeaways

Amidst prevailing worries of dwindling consumer expenditures, particularly in premium apparel segments, Lululemon stands its ground with a Zacks Rank #3 (Hold). The Q1 results serve as a testament to the promising earnings trajectory that lies ahead. Furthermore, trading at a modest P/E valuation of 22.9X, Lululemon appears primed for long-term investors to reap rewards, though greater buying opportunities may still lurk around the corner.