The Macerich Company MAC has rewarded investors with a sharp rally, but the buying case is no longer straightforward. The stock’s operating story has improved, while valuation and leverage leave less room for error.

For investors, MAC looks more like a selective hold than a clear bargain after its run. The question is whether future net operating income growth can justify further upside.

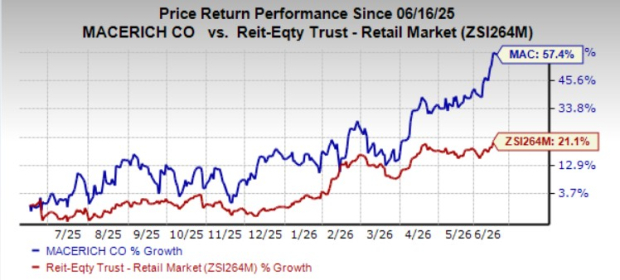

MAC Shows Strong Momentum but a Neutral Case

MAC shares are up 57.4% over the trailing 12-month period, outpacing the Zacks sub-industry’s 21.1% gain and the Zacks Finance sector’s 14.7% rise. That performance reflects better investor confidence in high-quality malls.

Image Source: Zacks Investment Research

The optimism is supported by leasing progress. Roughly 90% of go-forward net operating income comes from Class A properties, while go-forward portfolio occupancy was 94.5% as of March 31, 2026.

Simon Property Group SPG is a relevant peer because it owns premier shopping, dining, entertainment and mixed-use destinations. Tanger Inc. SKT also provides useful retail real estate context as an owner and operator of outlet and open-air shopping destinations.

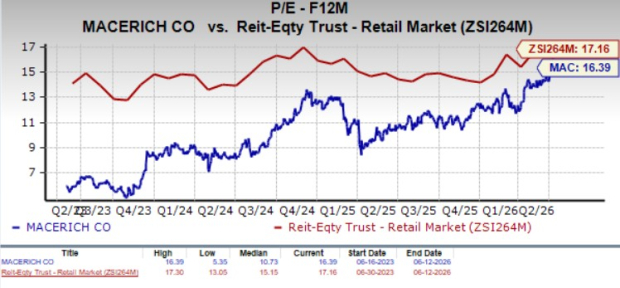

MAC Valuation Looks Fair, Not Cheap

MAC trades at 16.39X forward 12-month funds from operations. That is below the Zacks sub-industry’s 17.16X and the S&P 500’s 21.41X, but slightly above the Zacks sector’s 16.18X.

Image Source: Zacks Investment Research

The $27 price target, based on a 17.39X target multiple, points to limited incremental upside rather than a deep-value setup. MAC is not obviously expensive, but the rally has already priced in part of the recovery.

MAC Earnings Support Is Improving Slowly

First-quarter 2026 funds from operations, as adjusted, came in at 34 cents per share, matching the year-ago quarter and beating the Zacks Consensus Estimate by 9.68%. Revenues of $241.54 million declined 3.1% year over year but topped the consensus mark by 1.2%.

Estimate trends have improved only modestly. The current-year funds from operations estimate moved 1.2% higher over the past four weeks.

Management also lifted its 2028 target funds from operations range to $1.80-$2.00 per share. Still, annual estimates of $1.46 for 2026 and $1.56 for 2027 suggest measured progress rather than rapid earnings acceleration.

MAC Still Carries Leverage and Dividend Limits

Leverage remains the main counterweight. Net debt to adjusted EBITDA was 7.76X as of March 31, 2026, while pro forma leverage was about 7.26X after the Annapolis Mall acquisition and follow-on equity issuance.

Property-level issues also matter. The $76.5 million pro rata loan at Twenty Ninth Street was in default as of Feb. 6, 2026, with the joint venture still negotiating terms with the lender.

The dividend is another restraint. MAC paid 17 cents per share in the first quarter and announced another 17-cent quarterly dividend payable in June 2026, leaving limited near-term dividend growth while redevelopment and balance-sheet repair remain priorities.

What MAC’s Ratings Say About Timing

MAC’s operating recovery is real, but the stock looks closer to fairly valued than mispriced. Investors buying now are paying for continued leasing execution, higher occupancy and net operating income gains through 2028.

MAC currently carries a Zacks Rank #3 (Hold). That rank supports a wait-and-see approach rather than an aggressive buying stance. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores point in the same direction. MAC has a Value Score of C, Growth Score of D, Momentum Score of D and VGM Score of D. The Value Score suggests valuation is not a major red flag, but the weak Growth, Momentum and VGM scores favor selectivity for investors seeking stronger near-term ranking support.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Simon Property Group, Inc. (SPG) : Free Stock Analysis Report

Macerich Company (The) (MAC) : Free Stock Analysis Report

Tanger Inc. (SKT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.