Phibro Animal Health Corporation PAHC is drawing investor attention because its growth story is increasingly tied to Animal Health, the company’s largest and most strategically important business. The segment now anchors the revenue base, while vaccines, medicated feed additives (MFA) and nutritional specialties give Phibro multiple avenues for expansion.

The stock’s near-term setup depends on whether this segment can keep offsetting risks from regulation, currency swings and uneven demand in smaller businesses.

Here’s a look at Phibro’s stock performance over the past 12 months.

Image Source: Zacks Investment Research

PAHC’s Growth Engine Inside Animal Health

Animal Health accounted for 74% of Phibro’s total revenues in fiscal 2025, making it the company’s clear growth engine. The segment grew 36% from fiscal 2024, reflecting the strength of a broader product platform across MFAs, nutritional specialty products and vaccines. The company develops, manufactures and markets more than 550 product presentations in this business, giving it a wide base of customers and species exposure.

For investors, the focus is simple. If Animal Health continues to grow, it can help Phibro absorb volatility in Mineral Nutrition and Performance Products while supporting a higher-quality earnings base.

Phibro’s MFA Franchise Gets a Bigger Runway

Phibro’s MFA franchise remains central to the Animal Health story, with its leading Stafac/V-Max/Eskalin platform is approved in more than 30 countries. The integration of Zoetis Inc.’s ZTS MFA business has brought more than 37 established product lines marketed across approximately 80 countries, along with six manufacturing sites in the United States, Italy and China.

That broader footprint expands Phibro’s ability to serve customers across regions and supports a larger recurring revenue base. This added scale is important because it does not rely on a single product or geography.

PAHC’s Q3 Segment Mix Shows the Momentum

The fiscal third-quarter 2026 results showed how that platform is translating into revenue momentum. Animal Health net sales increased 13% year over year to $291.2 million, ahead of the internal model projection of $265.7 million.

The acquired MFA business generated a full quarter of revenues and grew 25% over the prior-year period. Legacy MFA sales increased 5%, helped by demand in North America and certain antimicrobials sold by the Ethanol Performance business. Nutritional specialty product sales rose 8% on higher North America demand and higher companion animal sales.

Vaccines net sales were up 16% year over year. That segment mix supported management’s updated fiscal 2026 outlook, including net sales of $1.46 billion to $1.50 billion and adjusted EBITDA of $247 million to $255 million.

Phibro’s Vaccines Add a Differentiated Growth Vector

Phibro’s vaccine business gives Animal Health a growth avenue that differs from mature feed additive categories. In fiscal third-quarter 2026, vaccine sales rose 16%, driven by higher international demand, including Israel, along with stronger domestic swine demand and increased sales of autogenous vaccines.

The business includes approximately 50 product lines for poultry disease prevention, covering areas such as Infectious Bursal Disease, Infectious Bronchitis, Newcastle Disease, Reovirus, Salmonella and Coryza. As disease pressures shift, vaccines can become a more differentiated part of the portfolio because they are less exposed to generic competition than some feed additive categories.

Phibro is also investing in vaccine manufacturing capacity, including its production facility in Guarulhos, Brazil. That capacity expansion supports volume growth and broader access across geographies.

PAHC’s Global Footprint Helps Smooth Species Cycles

Phibro’s international reach adds another layer to the Animal Health case. The company markets nearly 770 product lines in more than 80 countries to about 4,000 customers, with operations focused on regions where livestock production is concentrated in large commercial farms.

That strategy supports product adoption and recurring demand. In fiscal third-quarter 2026, net sales rose 14% year over year in Europe, the Middle East and Africa, 9% in Asia Pacific, and 7% in Latin America and Canada.

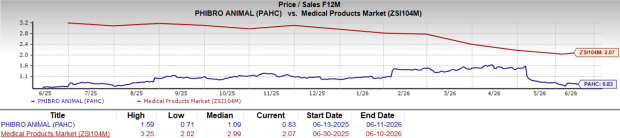

Take a look at Phibro’s valuation.

Image Source: Zacks Investment Research

Large peers such as Zoetis and Merck & Co., Inc. MRK also show how broad animal health platforms can benefit from scale, product depth and geographic reach, though Phibro’s mix remains more concentrated around its own feed additive, vaccine and nutrition strengths.

Phibro’s Outlook Balances Tailwinds With Known Risks

Phibro’s Health growth is being supported by the Zoetis MFA portfolio, steady legacy demand and higher vaccine volumes. Management also raised the low end of full-year expectations, a sign that recent execution has improved visibility. Yet, Brazil’s antimicrobial transition creates uncertainty for virginiamycin and bacitracin, while Mecadox remains under regulatory and legal scrutiny. Foreign exchange can also add earnings volatility, with fiscal third-quarter results including $1.9 million of foreign currency losses. Competition is another factor.

PAHC carries a Zacks Rank #2 (Buy), but the path is likely to remain uneven if Brazil disruption, currency pressure or generic competition weigh on the Animal Health growth engine.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Merck & Co., Inc. (MRK) : Free Stock Analysis Report

Zoetis Inc. (ZTS) : Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.