PVH Corp. PVH is trying to turn brand momentum into steadier profitability as apparel demand stays uneven. The company’s latest quarter showed progress in direct-to-consumer channels, digital commerce and inventory control.

The stock’s next move may depend on whether those gains can offset tariff pressure, weaker wholesale trends and softer demand in Europe, the Middle East and Africa.•

Direct-to-Consumer Channels Remain a Bright Spot

PVH’s direct-to-consumer business remains central to its growth strategy. In the first quarter of fiscal 2026, direct-to-consumer revenues increased 6% on a reported basis and 3% in constant currency, with growth across both Calvin Klein and Tommy Hilfiger.

Owned and operated stores rose 5% reported and 2% in constant currency. Owned and operated digital commerce grew 11% reported and 6% in constant currency, with gains across all regions.

The channel mix matters because wholesale remained under pressure. Wholesale revenues were flat on a reported basis but down 6% in constant currency, reflecting declines across regions and cautious partner behavior.

Ralph Lauren Corporation RL is a relevant peer for investors watching global apparel brands with direct-to-consumer and wholesale exposure. Tapestry, Inc. TPR, the parent of Coach and Kate Spade, offers another comparison point for branded consumer companies trying to deepen direct customer relationships while managing discretionary spending pressure.

AI and Data Tools Support Execution

PVH is investing in a more data-driven operating model under its PVH+ Plan. The company is using its enterprise data platform and Artificial Intelligence partnerships to improve consumer insights, demand forecasting and operational execution.

Management has linked these capabilities to faster decision-making across consumer, product and supply-chain areas. That is important in apparel, where inventory freshness, category timing and promotional discipline can quickly affect margins.

The company also completed more than 140 store refurbishments and openings combined in the first quarter. These investments are aimed at improving the consumer experience across stores, digital shop-in-shops and e-commerce.

PVH Corp. Price, Consensus and EPS Surprise

PVH Corp. price-consensus-eps-surprise-chart | PVH Corp. Quote

Margins Hold, but Tariffs Stay in Focus

PVH’s gross margin was 58.6% in the first quarter, flat with the prior year. That result came despite increased tariffs on goods entering the United States, a more promotional environment and margin pressure tied to bringing some previously licensed women’s categories in-house.

Tariff mitigation, favorable mix and lower product costs helped offset those pressures. Inventory also declined 5% year over year to $1.510 billion, giving PVH more flexibility as it manages demand shifts.

Non-GAAP operating margin was 6.5%, at the high end of guidance. For fiscal 2026, PVH reaffirmed its non-GAAP operating margin outlook of approximately 8.8%, flat with fiscal 2025.

Outlook Balances Momentum and Macro Pressure

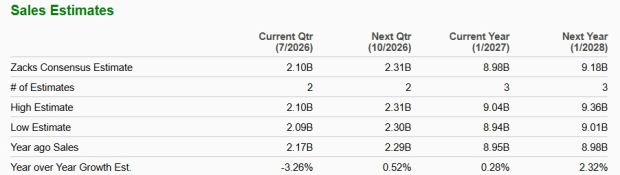

PVH reported first-quarter revenues of $2.025 billion, up 2% year over year on a reported basis but down 2% in constant currency. Adjusted earnings came in at $2.01 per share, above guidance, though lower than $2.30 in the prior-year quarter.

The full-year sales view remains cautious. PVH now expects fiscal 2026 revenues to be approximately flat on a reported basis and to decline slightly in constant currency.

Image Source: Zacks Investment Research

EMEA remains the main drag, with first-quarter constant-currency revenues down 5% due to softness in both direct-to-consumer and wholesale channels. The company expects the prolonged effects of the Middle East conflict to continue weighing on the region.

Tariffs add another layer of uncertainty. PVH’s outlook assumes a full-year blended tariff rate of roughly 15% on goods coming into the United States, with an estimated gross EBIT impact of about $195 million, or roughly 215 basis points of operating margin pressure. Tariff refunds are expected to provide a partial offset, including an estimated $100 million EBIT benefit.

Bottom Line on PVH Stock

PVH’s investment case is tied to execution. Direct-to-consumer growth, e-commerce gains, Artificial Intelligence-enabled planning and inventory discipline support the story, but flat sales guidance and tariff uncertainty keep the setup balanced.

PVH currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also has a VGM Score of A, a Value Score of A, a Growth Score of C and a Momentum Score of A. The Value Score of A and Momentum Score of A point to favorable valuation and share-price characteristics, while the Growth Score of C suggests a more measured growth profile. Combined with the Zacks Rank #3, PVH looks like a stock to monitor closely as investors assess whether digital gains and margin discipline can offset macro and tariff headwinds.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

PVH Corp. (PVH) : Free Stock Analysis Report

Tapestry, Inc. (TPR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.