Aerospace and defense manufacturers are operating in a complex environment shaped by uneven program funding, elevated input and labor costs and continued pressure from original equipment manufacturers (OEMs) to improve execution and reliability. In this backdrop, CPI Aerostructures, Inc. CVU and SIFCO Industries, Inc. SIF stand out as two players with distinct roles within the aerospace supply chain. CVU is primarily focused on complex structural assemblies, integrated systems and kitted solutions for military aircraft and defense platforms, functioning both as a supplier to major OEMs and as a prime contractor on select government programs. SIF, by contrast, specializes in forgings, machined components and sub-assemblies, serving aerospace, defense, commercial space and energy customers through a vertically integrated manufacturing footprint.

CPI Aerostructures’ business model offers exposure to long-duration defense programs and established military platforms, which can support revenue visibility but also introduce contract-specific execution and funding risk. SIFCO’s model is more manufacturing-driven, leveraging specialized forging and processing capabilities across multiple end markets, providing diversification but leaving results sensitive to broader aerospace production cycles and customer demand trends. With both companies tied to aerospace and defense spending but pursuing different strategies, scale and risk profiles, the key question is: which stock appears more attractive at this point? Let’s take a closer look.

Stock Performance & Valuation: SIF vs. CVU

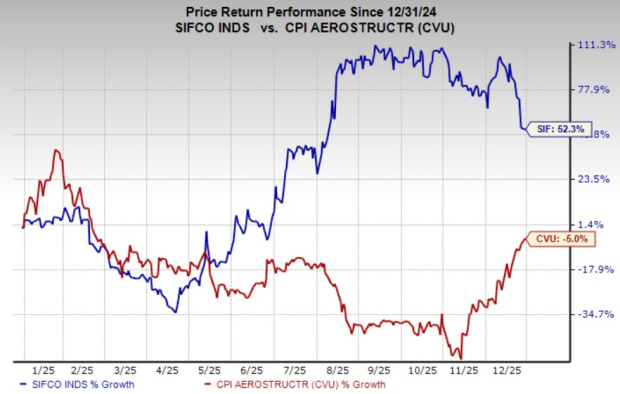

SIF (down 22.9%) has underperformed CVU (up 52.8%) over the past three months. However, in the past year, SIFCO has rallied 52.3% against CPI Aerostructures’ loss of 5%.

Image Source: Zacks Investment Research

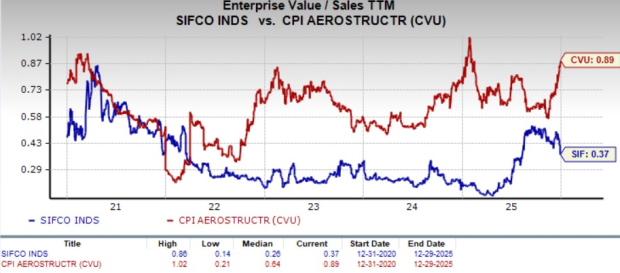

Meanwhile, SIF is trading at a trailing 12-month enterprise value-to-sales (EV/S) ratio of 0.37X, above its median of 0.26X over the past five years. CVU’s forward sales multiple sits at 0.89X, above its last five-year median of 0.64X. SIF and CVU both appear to be cheap when compared with the Zacks Aerospace sector average of 3.56X.

Image Source: Zacks Investment Research

Factors Driving SIFCO’s Stock

SIFCO’s stock is being driven by improving operating momentum as the company benefits from stronger demand across its aerospace and defense end markets. Management highlighted that demand has been solid in both military and commercial aircraft programs, supporting year-over-year sales growth and contributing to better overall financial performance. SIF also noted that customer demand for its forging solutions remains encouraging, reinforcing visibility into near-term production activity.

Another key driver is SIFCO’s ongoing margin-improvement strategy. The company is actively focused on cost reduction initiatives and selective price increases, and this operating discipline has supported improved profitability measures versus the prior year. This signals that performance is being shaped not only by demand recovery, but also by internal execution and tighter expense control.

Finally, SIFCO’s strategic streamlining has sharpened its focus on its core aerospace forging business. Following the sale of its European operations, the company has repositioned itself to concentrate resources on domestic operations and core capabilities, which management believes better aligns with long-term growth and stability goals.

Factors Driving CPI Aerostructures’ Stock

CPI Aerostructures’ stock is being supported by its growing exposure to long-duration defense and electronic warfare programs. The company continues to secure production and follow-on work on established military platforms, including pod structures, structural assemblies and systems tied to priority U.S. defense programs. These programs tend to run over multiple years and create a steady flow of contracted work, improving business visibility even as funding is staged over time.

Another key driver is CPI Aerostructures’ positioning as both a Tier 1 supplier and a prime contractor, which allows it to participate across multiple layers of the aerospace and defense supply chain. This dual role enables CVU to deepen relationships with major defense contractors while also bidding directly on government work, expanding its addressable opportunity set. Its focus on build-to-print manufacturing, integrated systems and value-added services aligns well with shifting customer preferences toward outsourcing complex assemblies.

Finally, CPI Aerostructures’ recent operational progress is helping stabilize investor sentiment. Management has emphasized improved execution, product mix and efficiency, which has supported profitability despite disruptions from program terminations and cost pressures earlier in the year. Ongoing balance sheet improvements and disciplined cost management further reinforce confidence in CVU’s ability to navigate near-term volatility while pursuing new program wins.

Choose SIF Over CVU Now

While both SIFCO Industries and CPI Aerostructures operate within the aerospace supply chain, their fundamentals point to two very different upside profiles — and the current setup favors SIF. CVU is benefiting from strong execution and continued traction in defense and electronic warfare programs, which have helped drive sharp stock gains in recent months. However, that momentum has also pushed its valuation above historical norms, suggesting that much of the near-term improvement is already being reflected in the price.

SIF, in contrast, offers a more attractive risk-reward entry point. Despite a strong rally over the past year, the stock has pulled back over the past three months, leaving it trading at a meaningfully low sales multiple relative to both its peer CVU and the broader aerospace sector. At the same time, SIFCO’s recovery is being supported by improving demand conditions across its end markets, margin-focused actions, and a streamlined operating structure. With valuations still inexpensive and operational progress continuing, SIF appears to offer greater upside potential from a re-rating perspective, making it the more compelling aerospace pick over CVU right now.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market’s next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don’t build. It’s just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>

CPI Aerostructures, Inc. (CVU) : Free Stock Analysis Report

SIFCO Industries, Inc. (SIF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.