Silicon Motion Technology Corporation SIMO has gained a stellar 307.4% over the past year compared with the industry’s growth of 221.9%. It has also outperformed peers like Advanced Micro Devices, Inc. AMD and International Business Machines Corporation IBM. While Advanced Micro has gained 284.2%, IBM has lost 1% over the same period.

One-Year SIMO Stock Price Performance

Image Source: Zacks Investment Research

SIMO Buoyed by Health Portfolio Traction

Silicon Motion has strengthened its position as the leading independent supplier of client SSD (solid-state drive) controllers to module makers, serving many of the top manufacturers across the United States, Taiwan and China. The company has worked closely with NAND flash vendors to develop proprietary controller technologies that address the limitations of 3D NAND architecture, enabling it to maintain a competitive edge. With initial shipments of its 3D SSD controllers already underway, Silicon Motion expects these products to become a key growth driver over the coming year as its flash partners continue expanding 3D NAND production capacity.

The company has also begun mass production of PCIe NVMe client SSD controllers for its flash partners, positioning itself to benefit from growing SSD demand and favorable industry dynamics. Further strengthening its portfolio, Silicon Motion introduced the industry’s first PCIe Gen5 client SSD controller, the SM2508, built on TSMC’s advanced 6nm EUV process. The controller delivers up to 50% lower power consumption than comparable 12nm solutions while offering as much as 1.7 times greater power efficiency than PCIe Gen4 SSDs.

Beyond client SSDs, Silicon Motion continues to broaden its market reach by expanding SSD controller programs with PC OEMs and increasing shipments of eMMC and UFS controllers for smartphones, automotive systems and IoT devices. The company is also preparing to launch its next-generation enterprise-class SSD controllers, which should further diversify its growth opportunities. Its eMMC business is showing encouraging signs of recovery, reinforcing the strength of its embedded storage portfolio. As the market shifts from legacy eMMC 4.5 to the more advanced eMMC 5.1 standard, Silicon Motion expects rising demand for its latest eMMC controllers to provide another meaningful avenue for growth.

Fabless Business Model Provides a Competitive Advantage

Silicon Motion operates under a fabless business model, concentrating on the design and development of semiconductor chips while outsourcing manufacturing to leading foundries such as TSMC. This approach significantly reduces capital expenditure by eliminating the need to invest in costly fabrication facilities. As a result, the company can rapidly adopt the latest manufacturing technologies, improve profitability through higher margins and dedicate greater resources to research, innovation and product development instead of managing manufacturing operations.

The company is well-positioned to benefit from several high-growth end markets, including artificial intelligence (AI), high-performance computing (HPC), cloud data centers, automotive storage and smartphones and other mobile devices. These markets continue to expand, creating substantial opportunities for the company. We believe Silicon Motion’s broadening customer base, coupled with its continued focus on developing innovative storage controller solutions, will support sustained revenue growth in the years ahead.

Image Source: Zacks Investment Research

SIMO Offers Bullish Guidance

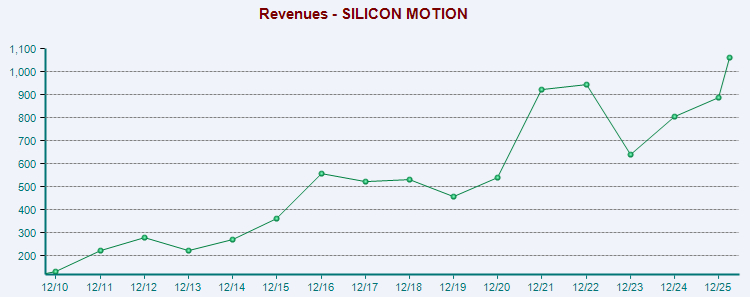

For the second quarter of 2026, Silicon Motion expects revenues in the range of $393 million to $411 million, representing sequential growth of 15% to 20% and year-over-year growth of 98% to 107%. Management expects continued momentum through 2026, supported by new product ramps, expanding enterprise opportunities and sustained market share gains across its core businesses.

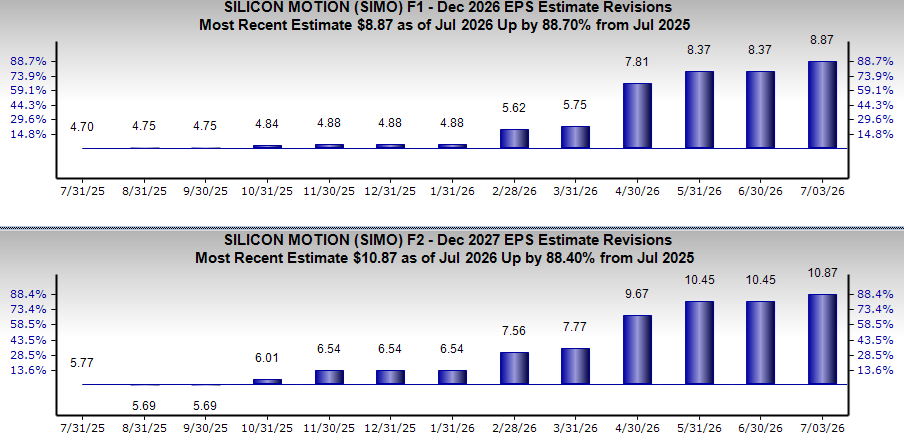

Estimate Revision Trend

Earnings estimates for Silicon Motion for 2026 have moved up 88.7% to $8.87 over the past year, while the same for 2027 have increased 88.4% to $10.87. The positive estimate revision depicts optimism about the stock’s growth potential.

Image Source: Zacks Investment Research

End Note

With solid fundamentals and healthy revenue-generating potential, driven by robust demand trends, Silicon Motion appears to be a solid investment proposition. Further, a strong emphasis on quality, diligent execution of operational plans and continuous portfolio enhancements are driving more value for customers. An asset-light fabless semiconductor model, solid growth exposure to AI, cloud and automotive markets, with increasing market share in SSD and mobile controllers and continuous innovation in storage technologies are key growth drivers for the company.

The stock has a long-term earnings growth expectation of 53.6% and delivered a trailing four-quarter average earnings surprise of 18.6%. Silicon Motion sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Riding on a robust earnings surprise history and favorable Zacks Rank, Silicon Motion appears primed for further stock price appreciation. Consequently, investors are likely to profit if they bet on this high-flying stock now.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Silicon Motion Technology Corporation (SIMO) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

International Business Machines Corporation (IBM) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.