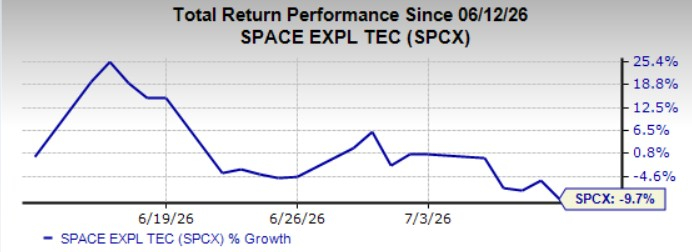

A month after SpaceX SPCX went public, many retail investors who bought in during the first week of trading are now sitting on losses.

When SPCX stock made its market debut on June 12, demand was overwhelming. Priced at $135, the stock opened at $150, climbed as high as $176, and closed its debut day at $160.95. The rally continued into the following week, with shares touching an intraday peak of $225 on June 16— a valuation that briefly pushed SpaceX past Amazon AMZN and Microsoft MSFT to become one of the world’s most valuable companies.

From there, the stock witnessed volatility—sharp drops followed by brief rebounds. When SpaceX joined the Nasdaq-100 index on July 7, it fell 6.8%. By the end of its first month of trading, shares slipped to a fresh all-time low of around $145— about 18% below its first-day high and roughly 35% off its all-time peak.

SPCX’s Run on the Bourses Since IPO

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

That leaves investors with a pressing question: how is SpaceX’s underlying business actually performing? Does this pullback represent a genuine buying opportunity or is it smarter to wait on the sidelines?

Starlink: SpaceX’s Cash Cow

Starlink— satellite broadband business— has emerged as the financial backbone of SpaceX. It’s now a global broadband business serving consumers across 164 countries and markets. As of March 31, 2026, the network supported approximately 10.3 million subscribers through a constellation of nearly 9,600 low-Earth orbit satellites, with peak download speeds of 225 Mbps.

The business is generating meaningful profits as well. Starlink’s connectivity segment generated more than $11.4 billion in revenues and $4.4 billion in operating income in 2025. Adjusted EBITDA reached $7.2 billion last year and $2.1 billion in the first quarter of 2026. The business has become cash-flow positive, providing SpaceX with a self-funded source of capital to support expensive initiatives, including Starship development and future satellite deployments.

There’s more growth ahead, too. SpaceX has spectrum rights and partnerships with about 30 mobile carriers worldwide, positioning Starlink to offer direct-to-phone text, voice, and data service— a huge expansion beyond traditional satellite broadband. On top of that, the next-generation V3 satellites, each capable of up to 1 terabit per second of downlink capacity, are set to start deploying in the second half of 2026.

With a high-margin subscription model, recurring revenues and expanding global demand for reliable connectivity, Starlink is likely to remain SpaceX’s primary earnings engine for years to come. But while it may generate the cash today, the company’s next phase of value creation could depend on something much bigger than broadband.

But Is Starship SpaceX’s Real Value Driver?

Starship is SpaceX’s fully reusable next-generation rocket, and that’s where the company’s long-term value proposition lies.

Unlike Falcon 9, Starship is designed to dramatically cut the cost of getting to space while carrying significantly larger payloads. If SpaceX pulls this off at scale, it opens doors that go well beyond satellite launches.

SpaceX completed Starship’s 12th integrated flight test in May and is already preparing for the 13th test on July 16. The upcoming mission will use the latest Starship and Super Heavy V3 vehicles powered by Raptor 3 engines. The relatively short gap between test flights reflects SpaceX’s strategy of learning quickly through frequent launches rather than waiting years between missions.

The end goal is a rocket that carries 100 to 150 metric tons to low-Earth orbit, with both the booster and spacecraft fully reusable. If reliability climbs and launch frequency increases, SpaceX expects launch costs to drop by orders of magnitude compared to today.

This matters directly for Starlink, too. Falcon 9 can only carry the smaller, compressed Starlink V2 Mini satellites. Starship, by contrast, is built to launch full-sized V2 and V3 satellites — meaning far more network capacity per mission, and lower costs per unit of bandwidth delivered over time.But Starship’s real significance goes beyond Starlink. A launch system that can move heavier payloads at a fraction of current cost could make entirely new categories of missions— commercial, government, deep-space— economically viable for the first time.

SpaceX’s AI Ambitions

SpaceX is also reinventing itself as an AI infrastructure player, following its acquisitions of xAI and X. By merging AI models, massive computing power and satellite networks, it’s building a combination that rivals struggle to replicate. Space-based data centers are on the roadmap, too, with AI compute satellites targeted for 2028.

This AI push is already paying off commercially. Large multi-year computing deals with Google and Anthropic give SpaceX steady future revenues, while its planned purchase of Anysphere— maker of the Cursor coding tool— deepens its foothold in enterprise AI software.

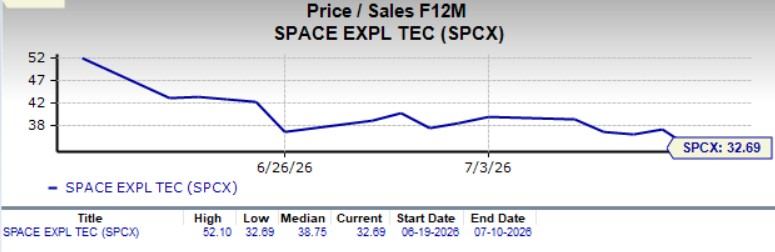

Are Valuation Concerns Valid or Overblown?

At roughly 32 times forward sales, SPCX stock certainly looks expensive by traditional metrics, even among high-growth tech peers. But judging SpaceX purely on current numbers risks repeating the mistake investors made with Tesla TSLA for years, dismissing it as overvalued while underestimating its execution and innovation.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Yes, many of SpaceX’s growth initiatives are still years away from making a meaningful financial contribution and will require huge investment before they begin generating attractive returns. But as Starlink keeps gaining traction and once Starship succeeds at scale, SpaceX could secure a multi-year monopoly in commercial space launch.

Our Take

SPCX stock isn’t a screaming buy at its current valuation, but it is also not worth dumping on panic either. The long-term thesis— Starlink’s cash-generating scale, Starship’s monopoly potential, and AI infrastructure pivot— remains intact. Wall Street’s average price target still implies roughly 62% upside from current levels.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Just as chasing this dip is premature, exiting the position is short-sighted. The smarter call right now is to hold and watch execution closely.

SPCX stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Space Exploration Technologies Corp. (SPCX) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Tesla, Inc. (TSLA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.