Michael Burry’s crash warning … the one macro risk that actually matters … why the earnings data tells a different story… where Louis Navellier and Luke Lango are investing today

Michael Burry has a message for investors who’ve been riding this bull market…

The end of… this… is nigh.

Last week, Burry – the investor made famous by the movie “The Big Short” – went on to say that “the market has jumped the shark,” and investors should “reject greed” while considering cutting their exposure to red-hot AI chip stocks “almost entirely.”

Here’s Burry’s overall sum-up:

Anyone lucky enough to be riding these parabolic moves, by not selling, is betting on one’s own ability to jump off at or near the top…

This, all of it, is the scene of the bloody car crash, minutes before it happens.

Now, Burry is an intelligent guy. But that doesn’t mean he’s right.

He’s made some famously wrong calls in recent years:

- His short bet against Tesla in 2021, which is highly likely to have resulted in a loss…

- His single-word post on X (formerly Twitter) in January of 2023 simply stated “SELL” – right before the market surged about 19% that year…

- His puts against the S&P in August of 2023 that he had to close out because the market kept climbing…

Still, it would be foolish to dismiss outright his claim that we’re “minutes” before the crash. After all, despite the “up” day in the market as I write on Wednesday morning, many of the hottest AI names that were setting all-time highs a week ago are now down double digits from those highs.

Are we already nanoseconds into the collision?

Another famous investor has a different read on today – Louis Navellier.

Let’s go to his Growth Investor Special Market Podcast from yesterday:

Yields have been meandering higher, and that is weighing on stocks.

We’re seeing inflation ripple through the economy, especially from higher shipping and travel costs.

So, the concern now is stagflation – slower growth with inflation pressures still bubbling through.

Burry would likely agree with this. But whereas Burry would go on to predict an imminent market meltdown, here’s Louis’ take:

I don’t want you to confuse today’s gyrations with a change in the bigger story. Earnings season has been stunning, and the AI boom remains intact…

This is just what happens as earnings season winds down – the profit-taking kicks in.

There’s no narrative out there or news to cause these selloffs…

The root question for bears predicting a bust: “why now?”

Here’s the thing about market crashes: they almost never happen simply because stocks are expensive.

Valuations can stay stretched for months – sometimes years. “Expensive” has a way of getting more expensive before the reckoning arrives – often long after when the crash was predicted to happen.

Older investors will recall 1996, when Alan Greenspan famously warned of “irrational exuberance” in the stock market. But from that warning, the S&P 500 nearly doubled over the next four years before the dot-com bubble finally burst.

Or consider 2017, when Burry himself and a chorus of other sharp minds called U.S. equities dangerously overpriced. The market climbed another 20% before so much as a serious correction.

The point isn’t that warnings and elevated valuations don’t matter. But something must trigger the AI trade’s unraveling.

Lofty P/E ratios set the kindling – but you need a match.

“Jeff, there are a zillion matches out there – Iran, oil prices, a Fed that won’t cut rates, tariffs, bond yields, you name it.”

Fair.

But let’s look zero in on the driver of today’s bull market – the AI trade – and then look at some of these matches through the lens of AI capex spending.

From this perspective, most of today’s macro concerns look more manageable than the headlines suggest

The reason is straightforward…

The hyperscalers have already collectively pledged hundreds of billions in AI infrastructure spending over the next 18 to 24 months. That capital doesn’t get pulled because oil prices rise or the Fed holds rates an extra quarter or two.

The spending is baked into budgets, construction timelines, and supplier contracts. So, for the companies sitting in the path of that spending – the chip designers, the data center builders, the power providers – there’s a known earnings pipeline that most macro shocks simply can’t derail.

Iran?

Painful for energy-intensive industries, for consumers at the pump, for airlines. But a Riyadh-Tehran conflict doesn’t make Microsoft cancel its next data center.

Oil with a new home above $90?

A headwind for broad corporate margins, absolutely – but not for the hyperscaler capex cycle driving AI earnings.

A hawkish Fed holding rates higher for longer?

It slows rate-sensitive sectors, squeezes housing, pressures smaller borrowers. It doesn’t alter the competitive calculus pushing every major tech company to spend aggressively on AI infrastructure or risk falling behind.

There is, however, one macro variable that cuts differently…

Bond yields.

When rising yields become a problem

Bond yields are a different animal.

When the 10-year Treasury climbs, it doesn’t just raise borrowing costs – it mechanically compresses the valuations of long-duration growth stocks by making their future earnings worth less in today’s dollars.

It also hands investors a genuine risk-free alternative to risky stocks. The higher yields go, the harder the math gets for AI names trading at premium multiples.

And bond yields that climb too high could eventually hurt the math behind data center loans, kneecapping the AI rollout.

So, where does the pain actually start?

Our technology expert, Luke Lango, editor of Innovation Investor, just presented his readers with a yield roadmap.

At current levels – above 4.5% – Luke sees “some small, short-term turbulence in markets, but nothing more.” The AI trade remains intact.

A push toward 4.8% to 5% would bring “more significant disruption” – Luke suggests a 5% to 10% pullback, but still nothing that breaks the uptrend.

Things get more serious with a 10-year interest rate above 5%.

Luke believes that a 10% to 20% correction is on the table in that case. He says the AI trade gets “hit hard, then rebounds the fastest on the recovery.”

Here’s Luke with what comes beyond that:

A break above 5.25% would start to short-circuit things.

The economy starts to crack. EPS estimates fall. Stocks fall into a bear market. The AI trade gets hit hard.

And a break above 5.5% would pretty much kill everything. A 30%-plus stock market crash.

As I write on Wednesday, the 10-year yield sits at 4.58% – in Luke’s “slightly uncomfortable but manageable” zone.

So, Burry may be right that the kindling is dry, but so far, the lightning strikes remain far off on the horizon.

The foil to the risk of higher bond yields – earnings growth

One more piece of this picture tends to get lost in the valuation debate.

Most valuation metrics are backward-looking by design. They measure today’s prices against yesterday’s earnings, revenues, or what have you.

But in a high-growth environment, such a comparison brings blind spots. You miss what’s actually happening now as well as what’s likely to come tomorrow – and for a meaningful slice of this market, “what’s happening” is a surge in earnings.

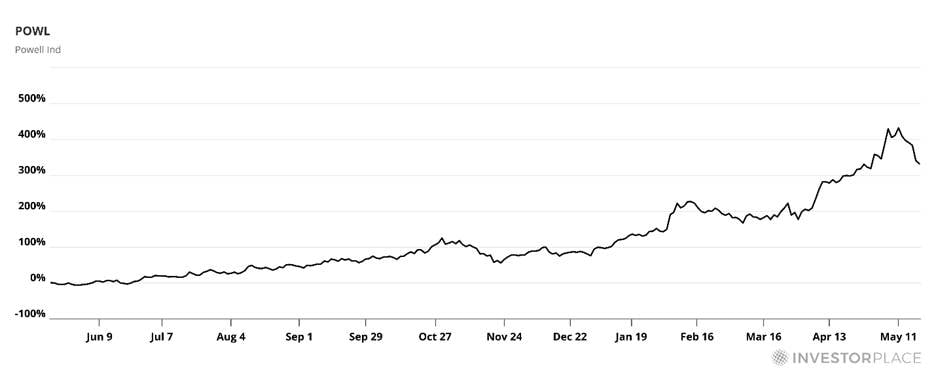

Consider Powell Industries (POWL) – a stock I own that makes specialized electrical switchgear and power systems. It’s squarely in the path of the AI data center buildout.

As you can see below, POWL is up more than 300% over the last year, even after the recent profit taking.

Given this price surge, a nosebleed valuation seems like a safe assumption. But it’s more complicated than that.

Depending on which financial website you visit and which earnings period it uses, POWL’s trailing P/E ranges from the low 30s to the mid-50s. That’s an unusually wide spread for a single stock.

What this spread reveals is that earnings have been growing so fast that even a slight discrepancy in the chosen earnings period can produce a dramatically different picture.

Neither number is wrong. They’re just measuring different versions of the same rapidly transforming business, though the 33 P/E is more accurate today.

And here’s the part that doesn’t show up in any trailing P/E calculation yet…

New orders last quarter totaled $490 million, up 97% year over year. Then, after the quarter closed, came a single “mega order” from an AI data center project worth $400 million. That revenue hasn’t yet appeared on the income statement. When it does, it will compress the multiple further.

The backward-looking metrics can’t capture a business being transformed in real time. That’s the point.

Now, detractors might say, “That’s just one company.” But zoom out, and the broader picture looks similar.

This is the story that bears won’t tell you today

According to FactSet’s latest Earnings Insight report, the S&P 500 just posted its highest earnings growth rate since Q4 2021 – 27.7% year-over-year, with 84% of companies beating estimates.

That beat rate is the highest since Q2 2021. Even more striking, companies are reporting earnings 17.9% above expectations – nearly two-and-a-half times the five-year average surprise of 7.3%.

And the S&P 500’s net profit margin just hit 14.7% – a record high since at least 2009, surpassing the prior record set just last quarter.

That’s not a market running on fumes and hope. That’s a market where earnings are legitimately catching up with – and in many cases outrunning – prices.

Yes, beware surging bond yields. But equally, yes, factor your stocks’ earnings growth into your market decisions.

So, what’s the verdict on Burry’s bearishness?

Burry may be right. But let’s complete our analysis with two missing pieces.

Regular Digest readers will recall – and for newer readers, it’s worth noting – a story we covered last November in which Burry closed his fund and returned capital to shareholders.

Why?

Because over the prior two years, while Burry had expected and positioned for dramatic pullbacks, the Nasdaq returned almost 70%.

From Burry to his investors:

My estimate of value in securities is not now, and has not been for some time, in sync with the markets.

This seems an appropriate time to remember the wise words of the legendary fund manager Peter Lynch:

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

Burry could be right. Eventually, some bear always is.

But a warning about stretched valuations, without a credible near-term catalyst to trigger the unraveling, is not a timing call – it’s a market disposition. And dispositions don’t tell you when to sell.

What does tell us something is the 10-year yield, the earnings trajectory of the specific companies you own, and the durability of the capex cycle underneath them.

That’s the framework worth watching right now – and it’s exactly what Louis and Luke are tracking for their readers every week.

So, while Burry is bearish, here’s Louis’ message to investors:

You basically want to buy good stocks on dips. Period.

For the latest “good stocks” that he’s recommending investors buy on dips, you can access his recent market briefing here.

As for Luke, here’s his bottom line:

Overall, we remain very bullish on the AI trade despite recent inflation/oil/rate jitters. The inflation/oil/rate jitters are creating just another run-of-the-mill pullback in a still-very-much-alive AI bull market.

Stick with the AI trade. Patience and resolve are the name of the game right now.

For what has Luke excited today – what he believes could be Elon Musk’s most ambitious project yet (it has nothing to do with Tesla or SpaceX) – click here for his full presentation.

Have a good evening,

Jeff Remsburg

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.