Key Points

-

Meta Platforms’ advertising business accounted for nearly 98% of its total revenue.

-

Meta is working to become a more vertically integrated artificial intelligence (AI) company.

-

Investors are skeptical about Meta’s capital expenditure plans for the year.

- 10 stocks we like better than Meta Platforms ›

The “Magnificent Seven” collectively refers to Nvidia, Apple, Microsoft (NASDAQ: MSFT), Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL), Meta Platforms (NASDAQ: META), and Tesla. They are among the most influential companies globally, from a business and stock market standpoint. As of the end of March, they accounted for over 32% of the S&P 500.

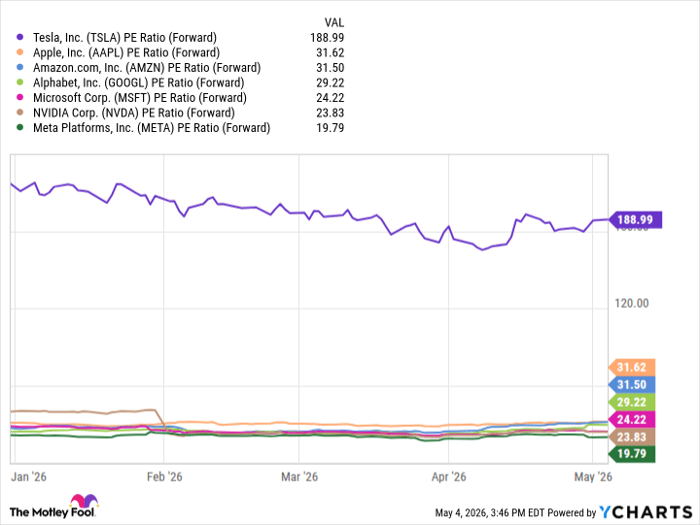

It’s often hard to find true value in a Magnificent Seven stock because of their popularity, but Meta is one that’s sliding into value territory. As of market close on May 4, it was trading at 19.8 times its projected earnings over the next 12 months — the lowest valuation of the group.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

TSLA PE Ratio (Forward) data by YCharts.

However, just because a stock is cheap doesn’t necessarily make it a good investment. Meta’s stock is down nearly 6% this year, but is it due to bad business performance and a weak outlook, or is it due to the market undervaluing the company? I believe it’s much more of the latter.

The ad business is still going strong

Meta’s core business has always been and continues to be advertising. In the first quarter, Meta’s advertising revenue was $55 billion, up 33% year over year, and accounted for nearly 98% of its total revenue.

This jump in advertising revenue was aided by a 19% increase in ad impressions and a 12% increase in average price per ad. People are watching Reels longer on Instagram and videos longer on Facebook.

Most big tech giants have one main engine that generates tons of income, which in turn allows them to fund their other ventures. In Meta’s case, its advertising cash cow has allowed it to invest in (often long-shot) projects like the Metaverse and virtual reality headsets. Now, that cash is going toward its artificial intelligence (AI) push.

The path to becoming a vertical AI company

Meta doesn’t usually get the same level of attention for its AI-related efforts as companies like Amazon, Microsoft, and Alphabet because it doesn’t operate a major cloud infrastructure platform. In fact, it signed a six-year, more than $10 billion deal with Alphabet last year that allows it to use Google Cloud’s computing power to run and train its AI models.

However, the release last month of Meta’s newest AI model, dubbed Muse Spark, is a sign the company should be taken a bit more seriously in the AI world. As Meta describes it, Muse Spark is “scaling toward personal superintelligence.” It outperforms more common models (like GPT, Gemini, and Grok) in a handful of areas, but what matters most for an AI model is its adoption, and with only a month since its debut, how that will play out remains to be seen.

Meta has also begun developing custom application-specific integrated circuits in partnership with Broadcom. It will still need to rely on companies like Nvidia and AMD for GPUs, but developing AI chips in-house will reduce its dependence on them, and offer it a way to begin cutting its computing costs. The company’s goal is to become vertically integrated as quickly as possible and gain greater control over its own AI ecosystem.

This doesn’t come cheap, though, which brings us to our next point.

Why investors aren’t embracing Meta as much as you’d think

Meta turned in a strong Q1 performance that beat analysts’ expectations, so why is the stock still struggling this year? It mostly comes down to Meta’s capital expenditure plans.

Meta said it expects to spend between $125 billion and $145 billion on capital expenditures this year, with most of that going toward constructing new data centers and other AI infrastructure. Its previous estimated range was $115 billion to $135 billion, a spending forecast that itself had drawn some understandable skepticism from investors.

Meta has made some notable missteps (like its massive money-losing bets on the metaverse), so it doesn’t necessarily get the benefit of the doubt when it comes to seemingly excessive spending. However, this time, it is not engaging in a company-specific strategy — most Magnificent Seven companies have similarly major AI infrastructure spending plans.

Even with the increase to its budget, Meta’s projected capex for the year is lower than Amazon’s ($200 billion), Alphabet’s ($175 billion to $185 billion), and Microsoft’s ($190 billion).

In my view, it would be much better for a tech giant to overspend in the AI race and not get left behind than to underspend and get left trying to play catch-up for who knows how long. At its current levels, Meta’s stock has much more long-term upside than downside.

Should you buy stock in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $473,985!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,204,650!*

Now, it’s worth noting Stock Advisor’s total average return is 950% — a market-crushing outperformance compared to 203% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 7, 2026.

Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Apple, Broadcom, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.