Alibaba BABA believes accelerating AI cloud demand could become the primary driver of enterprise growth in FY2027 as the commercialization of its AI infrastructure and model services gains momentum. During the fourth quarter of fiscal 2026, Cloud Intelligence Group’s external revenue growth accelerated 40% year over year, supported by triple-digit AI-related revenue growth for the 11th consecutive quarter. AI products now account for nearly 30% of external cloud revenues and are expected to exceed 50% within about a year.

On May 20, Alibaba unveiled a full-stack AI upgrade at its Alibaba Cloud Summit in Hangzhou, introducing the Qwen3.7-Max large language model, the Zhenwu M890 AI chip and the Panjiu AL128 Supernode Server for large-scale AI training and inference. The company mentioned that Qwen3.7-Max operated autonomously for 35 hours and executed more than 1,000 tool calls in benchmark testing. Alibaba also revealed the Zhenwu V900 and Zhenwu J900 chips, slated for the third quarter of 2027 and the third quarter of 2028, respectively. The launch strengthens Alibaba’s AI cloud demand outlook by expanding its in-house AI infrastructure, improving enterprise AI performance and attracting more customers seeking advanced agentic AI computing solutions on Alibaba Cloud.

Alibaba emphasized that enterprise demand is rapidly shifting from basic chatbot usage toward large-scale AI agents, inference and orchestration workloads. Management noted that token consumption on its Model Studio platform increased substantially as customers moved from testing AI applications to production-scale deployments. The company expects model and application services ARR to reach RMB 30 billion by the end of calendar 2026, highlighting the growing contribution of high-margin MaaS and AI-native software offerings.

The company also sees strong competitive advantages from its vertically integrated AI infrastructure. Alibaba stated that its proprietary T-Head AI chips already support scaled MaaS production, with more than 60% of compute capacity serving external customers across the internet, finance and autonomous-driving sectors. This self-developed chip capability strengthens supply-chain control while supporting both revenue growth and margin expansion amid industrywide compute shortages.

Management further highlighted that AI coding and enterprise productivity applications are becoming major growth catalysts in China. Notably, the most recent utilization growth on the Model Studio platform has been driven by improvements in coding and reasoning capabilities, enabling AI systems to solve increasingly complex workplace tasks across digitalized industries. The Zacks Consensus Estimate for the company’s fiscal 2027 revenues is pegged at $166.24 billion, indicating a year-over-year increase of approximately 14.3%.

However, FY2027 growth may depend on Alibaba’s ability to balance aggressive AI investments with profitability. Free cash flow turned negative, driven by heavy investment in both quick commerce and AI cloud infrastructure, while management acknowledged that capital expenditures could exceed prior targets as AI demand continues surging.

How Alibaba Fares Against Rivals

JD.com JD trails Alibaba in AI cloud demand and commercialization scale. Alibaba has positioned AI cloud services as a core enterprise growth engine, reporting 40% external cloud revenue growth and triple-digit AI revenue expansion driven by MaaS, AI agents and proprietary chips. In contrast, JD focuses on AI primarily for retail efficiency, logistics automation and advertising optimization rather than building external cloud monetization at scale. Alibaba currently holds a stronger position in China’s enterprise AI infrastructure and cloud ecosystem.

PDD Holdings PDD trails Alibaba in AI cloud demand exposure because PDD’s investments are concentrated on supply chain optimization, fulfillment efficiency, marketing algorithms and platform infrastructure rather than enterprise cloud services. While PDD increased R&D spending by 30% in 2025, mainly for staff, bandwidth and server costs, it lacks a large-scale public cloud ecosystem comparable to Alibaba Cloud. Alibaba, therefore, remains significantly better positioned to monetize rising enterprise AI computing and cloud demand globally.

BABA’s Share Price Performance, Valuation & Estimates

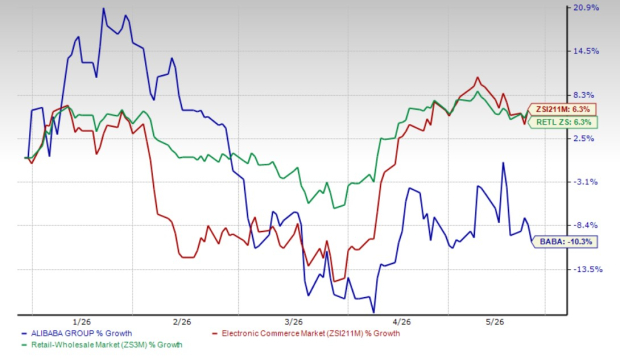

BABA shares have declined 10.3% in the year-to-date period, underperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 6.3% and 6.3%, respectively.

BABA’s YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, BABA stock is currently trading at a forward 12-month Price/Earnings ratio of 16.75X compared with the industry’s 23.91X. BABA has a Value Score of D.

BABA’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $7.43 per share, down 4.6% over the past 30 days and indicating a 91% year-over-year increase.

Image Source: Zacks Investment Research

Alibaba currently has a Zacks Rank #4 (Sell). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

JD.com, Inc. (JD) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

PDD Holdings Inc. Sponsored ADR (PDD) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.