Alignment Healthcare, Inc. ALHC is drawing investor attention as Medicare Advantage growth, quality ratings and operating leverage begin to show up in profitability. The company reported first-quarter 2026 earnings of 5 cents per share, compared with a year-ago loss.

The setup is still early. Alignment raised its full-year 2026 membership and revenue outlook, yet utilization, revenue timing and execution risks remain meaningful.

Why Alignment Healthcare Still Has Room to Grow

Alignment’s growth case starts with scale. Total membership increased 30.9% year over year to roughly 284,800 in the first quarter of 2026, helped by Medicare Advantage gains and higher per-member revenue tied to CMS benchmarks and Part D.

That prompted management to lift full-year 2026 guidance to 294,000-299,000 members and total revenues of about $5.160-$5.205 billion. The company still has a relatively small presence in many existing markets, giving it room to capture share without depending entirely on new-state expansion.

Molina Healthcare, Inc. MOH offers a useful comparison as another managed-care name tied to government-sponsored health programs. For ALHC, the narrower Medicare Advantage focus makes plan quality and local execution central to growth.

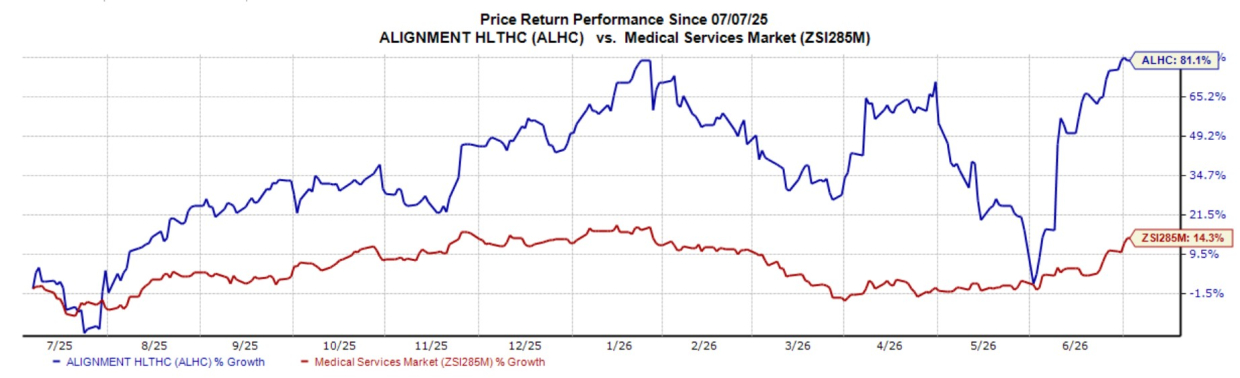

ALHC’s share price rose 81.1% in the past year compared with the industry’s 14.3% growth.

Image Source: Zacks Investment Research

ALHC Leans on Quality and Retention

Quality ratings remain a key part of Alignment’s competitive position. For the 2026 rating year, 100% of members are enrolled in plans rated 4 stars or higher, supporting visibility into the 2027 enrollment cycle.

The California health maintenance organization has maintained a 4-star-plus rating for nine consecutive years. That track record can support retention and enrollment competitiveness in a crowded Medicare Advantage market, where plan quality helps determine how effectively a carrier can attract and keep higher-value members.

How ALHC Is Turning Scale Into Margin Lift

The margin story is increasingly tied to automation. Claims auto-adjudication exceeded 60% in the first quarter of 2026, up from less than 15% a year earlier, while AI-enabled workflows are being applied to back-office operations, contract management and risk stratification through the AVA platform.

The operating impact is visible. Adjusted selling, general and administrative expenses declined 60 basis points as a percentage of revenues in the first quarter, while adjusted EBITDA margin expanded 90 basis points. Adjusted EBITDA rose 87.6% year over year to $37.9 million.

Surgery Partners, Inc. SGRY sits in the broader medical services space, with a different model built around surgical facilities and ancillary services. That contrast underscores ALHC’s focus on care management, automation and medical cost control.

Alignment Healthcare Faces Real 2026 Risks

Utilization is the biggest near-term test. Alignment intentionally added higher-acuity members in 2026, including growth in its Chronic Condition Special Needs Plan membership, and first-quarter admissions ran in the high-150s per 1,000 members.

The final phase-in of the CMS V28 risk adjustment model also reduces visibility. Alignment books revenues only from paid Monthly Member Revenue and does not assume new-member final sweep payments in guidance, which is prudent but can delay recognition of upside.

Product economics add another constraint. PPO plans remain difficult to operate profitably without higher member premiums, and management has not yet identified a sustainable model that consistently produces attractive economics.

Operational complexity is rising at the same time. A January authorization workflow issue tied to observation versus inpatient stays created an estimated 30-basis-point headwind to the first-quarter medical loss ratio before being resolved by late February.

In the past 30 days, the company’s earnings per share have remained unchanged at 20 cents.

Image Source: Zacks Investment Research

What ALHC Signals Say About the Setup

The bottom line is that ALHC has a growth-led setup with improving fundamentals, but the margin path still depends on execution. Membership gains, quality ratings and automation are working in the company’s favor, while higher-acuity utilization and revenue timing can make quarterly progress uneven.

The stock currently carries a Zacks Rank #1 (Strong Buy). Its Zacks Style Scores include a Growth Score of A, Value Score of D, Momentum Score of D and VGM Score of B.

That combination supports the view that ALHC is most attractive as a growth story rather than a value or momentum call. The VGM Score of B is favorable when viewed alongside the top Zacks Rank, but weaker Value and Momentum Scores temper expectations after a sharp share-price run.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Alignment Healthcare, Inc. (ALHC) : Free Stock Analysis Report

Molina Healthcare, Inc (MOH) : Free Stock Analysis Report

Surgery Partners, Inc. (SGRY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.