Alibaba Group BABA stock has clawed back some ground in July, but the year-to-date (YTD) scoreboard still tells an unflattering story, and investors weighing whether to hold on or lock in relief are staring at a business whose near-term fundamentals remain considerably shakier and more uncertain than the recent bounce off multi-month lows would otherwise suggest.

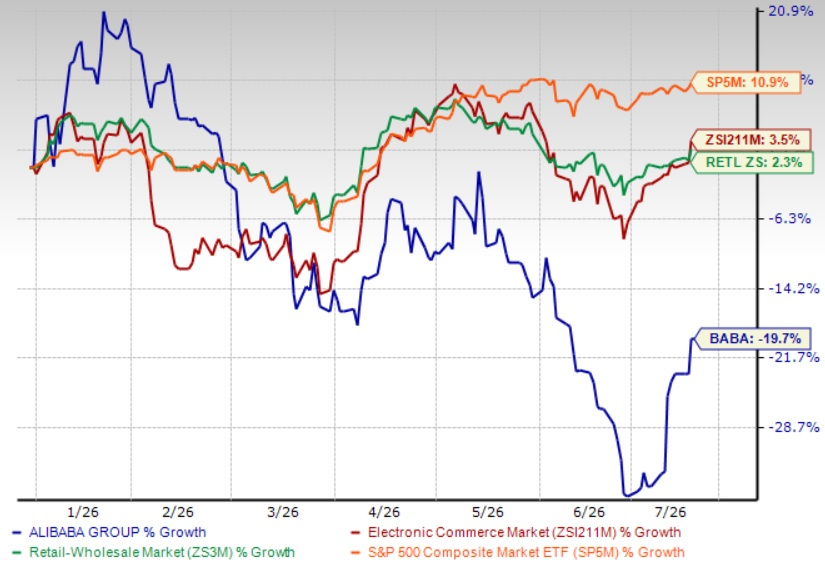

BABA shares have plunged 19.7% YTD, underperforming the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 3.5% and 2.3%, respectively.

BABA Underperforms Industry, Sector YTD

Image Source: Zacks Investment Research

Recent Headwinds Add to the Uncertainty

Alibaba’s recent news flow has been a mixed bag that leaves little room for comfort. In July 2026, the company detailed a $600 million non-prosecution settlement with the U.S. Department of Justice tied to historical sales of illegal pharmaceutical products on its marketplaces, resolving a long-running legal overhang. A U.S. district court granted Alibaba a temporary stay from a Pentagon rule, allowing continued lobbying, even as the Department of Defense’s blacklist labeling it a Chinese military-linked company remains in force and could restrict procurement-related business. Shares got a lift after Chinese regulators approved the integration of Alibaba’s Qwen AI model into Apple Intelligence features in China, a rare bright spot. However, the company drew fresh scrutiny in June and July after Anthropic alleged Alibaba-linked accounts used fake profiles to extract capabilities from its Claude models, prompting Alibaba to curb internal use of rival AI tools. Separately, several law firms launched shareholder investigations.

Q4 Guidance Signals More Pain Ahead

Alibaba’s fourth-quarter fiscal 2026 results, reported in May, underscored the same tension between growth and profitability. Revenues rose just 3% year over year to RMB243.4 billion, missing estimates, though growth reached 11% on a like-for-like basis excluding divested assets. Adjusted EBITA collapsed sharply by 84%, and the company posted its first operating loss since early 2021, as heavy AI and quick-commerce spending overwhelmed core profitability. Cloud Intelligence Group revenues accelerated to roughly 38-40% growth, with AI-related products now representing about 30% of external cloud revenues. Management guided that AI product revenues are expected to cross 50% of cloud revenues within about a year, and cautioned that capital expenditure will likely overshoot its original RMB380 billion target given surging infrastructure needs. Free cash flow turned negative during the quarter. While management framed the spending as necessary for long-term AI opportunity, the guidance points to continued margin pressure and cash burn ahead.

The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $6.89 per share, down 5.5% over the past 30 days, indicating a 77.12% year-over-year increase.

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Valuation and Competitive Landscape

From a valuation standpoint, BABA stock is currently trading at a trailing 12-month Price/Earnings ratio of 37.24X compared with the sector’s 29.15X. BABA has a Value Score of C, reflecting a premium multiple relative to peers.

BABA P/E TTM Ratio Depicts Stretched Valuation

Image Source: Zacks Investment Research

Beyond the operational overhangs, Alibaba’s cloud ambitions face intensifying competition. Alibaba Cloud continues to expand across Asia, but it remains far smaller globally than Microsoft MSFT, Alphabet GOOGL-owned Google, and Amazon AMZN, each of which is deploying tens of billions of dollars in AI infrastructure annually. Microsoft’s Azure and Google’s Cloud platform both continue posting robust growth alongside deep enterprise AI partnerships, while Amazon’s AWS remains the largest hyperscaler by revenues, giving all three greater scale to absorb heavy capital spending than Alibaba has. Microsoft and Google enjoy diversified, cash-generative core businesses that cushion their AI investment cycles, whereas Alibaba’s e-commerce base is under domestic pressure from Chinese rivals. Amazon’s logistics and retail scale complicate Alibaba’s international commerce ambitions. Given persistent margin erosion, negative free cash flow and geopolitical restrictions limiting access to advanced chips, Alibaba’s competitive position against these three cloud leaders looks stretched, reinforcing caution around the stock in the near term.

The Bottom Line

Taken together, the fiscal fourth-quarter miss, the operating loss and management’s acknowledgment that capital spending will overshoot guidance suggest profitability pressure is unlikely to ease soon. Add to that the DOJ settlement costs, the ongoing Pentagon blacklist risk, fresh shareholder litigation and intensifying competitive spending from far larger, better-capitalized cloud rivals and the near-term risk-reward for BABA looks unfavorable.

The stock’s 19.7% year-to-date decline reflects concerns rather than sentiment, and with free cash flow negative and margins compressing even as AI investment accelerates, near-term catalysts for a sustained rebound appear limited. Long-term believers in Alibaba’s AI and cloud ambitions may choose to stay invested, but for investors focused on near-term performance, the combination of weak profitability, geopolitical overhang and heavy ongoing capital commitments makes booking profits or simply staying on the sidelines the more prudent near-term course rather than holding through uncertainty. Alibaba currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.