DoubleVerify Holdings, Inc. DV presents a split investment case. The stock trades at a low multiple, solid profitability and ongoing investment in social, connected TV and AI products.

The caution is growth. Revenue expansion has slowed from prior levels, and pricing pressure remains visible even as transaction volumes rise.

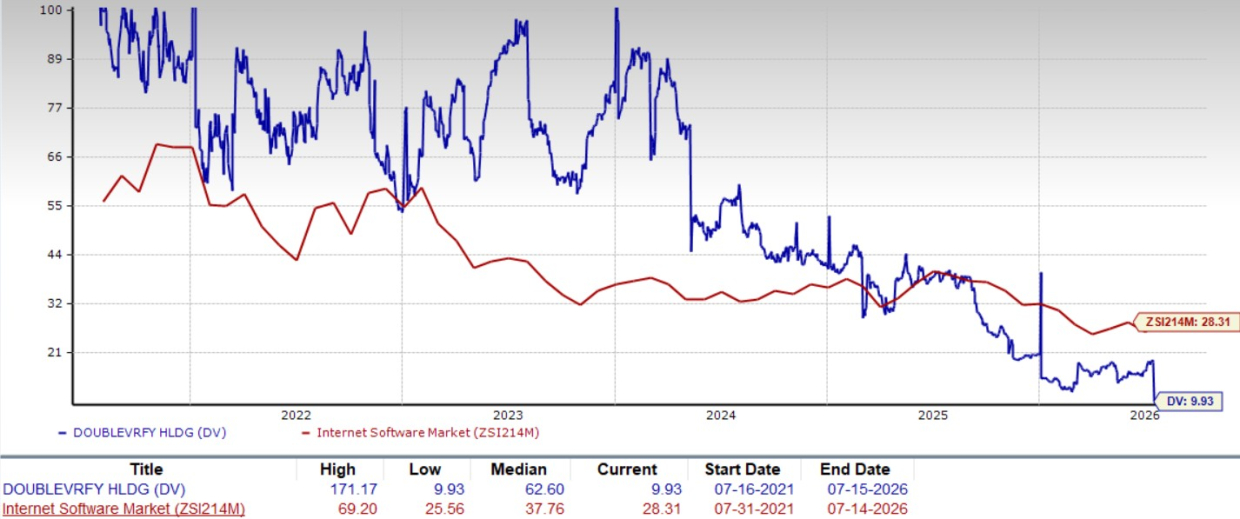

DV Valuation Looks Compressed

DV trades at 9.93X forward 12-month earnings, below 28.31X for the Zacks sub-industry, 24.49X for the Zacks Computer and Technology sector and 21.13X for the S&P 500.

That discount is also meaningful against its own history. Over the past five years, DV has traded as high as 171.17X and as low as 9.93X, with a median of 62.60X.

DoubleVerify Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

For investors seeking a lower-multiple software name, that setup can look appealing. The valuation already reflects a large amount of skepticism, while the company still has earnings growth potential.

DoubleVerify Still Delivers Healthy Margins

Profitability remains the clearest support for the bull case. In the first quarter of 2026, DV reported adjusted EBITDA of $55.2 million, equal to a 31% adjusted EBITDA margin.

The company also expects a full-year adjusted EBITDA margin of about 34%. That level of margin discipline helps offset part of the concern around slower revenue growth.

AI-driven efficiencies are playing a role in cost control. Management has tied margin expansion to operating efficiency, faster product launches and the broader use of AI across the business.

DV Growth Is Slowing From Prior Levels

DV’s revenues increased 10% year over year to $180.8 million in the first quarter of 2026. That still reflects growth, but it is below the company’s stronger 2025 revenue growth rate of 14.7%.

The second-quarter outlook points to further moderation. Management expects revenues of $199-$205 million, representing year-over-year growth of about 7% at the midpoint.

For 2026, DV expects revenues of $810-$826 million, implying growth of 8-10%. That makes execution in social, connected TV and AI products central to the debate over whether the valuation discount is justified.

DoubleVerify Faces Fee and Mix Pressure

The pricing picture is less favorable than the volume picture. Advertiser revenues represented 90% of total revenues and grew 9% year over year in the first quarter, while Media Transactions Measured increased 12%.

That volume gain was partly offset by a 4% decline in the fee charged per thousand measured transactions. Lower measured transaction fees can dilute the quality of revenue growth.

This dynamic makes product mix more important. DV needs scale, but it also needs greater adoption of higher-value offerings to reduce the drag from lower fee rates.

Competition adds to that pressure. comScore, Inc. SCOR is another audience measurement and media planning provider, while The Trade Desk, Inc. TTD is a major demand-side platform in the programmatic advertising ecosystem.

DV’s Balance Sheet Supports the Bull Case

Financial flexibility remains a real strength. DV ended the first quarter with approximately $174 million in cash and no debt outstanding.

The company has also been active with buybacks. It repurchased 9.8 million shares for $100.2 million year to date and still had $200 million authorized for repurchases.

That balance sheet does not remove execution risk, but it gives DV room to invest in AI and product expansion while returning capital.

What DV’s Ratings Say About Timing

The bottom line is that DV looks inexpensive and profitable, but the growth profile is not yet strong enough to make the timing straightforward. A low multiple can support interest, while slower growth and fee pressure argue for patience.

The stock currently carries a Zacks Rank #3 (Hold). That fits a balanced view, suggesting the shares are interesting but not a clear near-term conviction call. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DV also has a VGM Score of B, along with a Value Score of B and a Growth Score of B. Those grades point to attractive underlying value and growth characteristics.

The Momentum Score of F is the offset. Since Style Scores are meant to complement the Zacks Rank, investors may prefer stronger momentum or improved estimate stability before taking a more aggressive stance.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

DoubleVerify Holdings, Inc. (DV) : Free Stock Analysis Report

comScore, Inc. (SCOR) : Free Stock Analysis Report

The Trade Desk (TTD) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.