Delta Air Lines DAL) and United Airlines UAL) have both delivered better-than-expected Q2 results, demonstrating that demand for premium, international, and corporate travel remains resilient despite significantly higher fuel costs.

Both carriers exceeded Wall Street’s earnings expectations and expressed confidence in the second half of the year. However, they took slightly different approaches to guidance.

Delta reaffirmed its full-year outlook despite the challenging fuel environment, while United became even more optimistic by raising its earnings forecast.

For those looking to capitalize on the continued strength in the airline industry, the question is whether Delta’s operational consistency or United’s accelerating earnings momentum makes for the better investment.

Delta Delivered Another Strong Quarter

Last Friday, Delta reported Q2 adjusted EPS of $1.56, topping expectations of $1.51 despite an expected dip from last year’s record Q2 profit of $2.10 per share.

This came on a quarterly peak in revenue at $17.66 billion, which increased 14% year over year but slightly missed estimates of $17.76 billion. Premium travel, corporate demand, and international routes remained key growth drivers.

The quarter was particularly impressive considering Delta absorbed the highest quarterly fuel expense in company history, with fuel costs surging roughly 77% from a year ago due to higher oil prices. Despite the headwind, Delta generated approximately $1.4 billion in adjusted pre-tax income while maintaining an industry-leading balance sheet.

Perhaps most encouraging was management’s outlook. Delta reaffirmed its full-year adjusted EPS guidance range of $6.50-$7.50 while maintaining expectations for $3 billion-$4 billion in free cash flow.

Management also projected continued momentum during the September quarter, expecting double-digit operating margins as premium demand remains healthy. Delta further rewarded shareholders by announcing a 15% dividend increase.

Image Source: Zacks Investment Research

United Raises the Bar

Reporting Q2 results this week, United Airlines posted the more bullish earnings report.

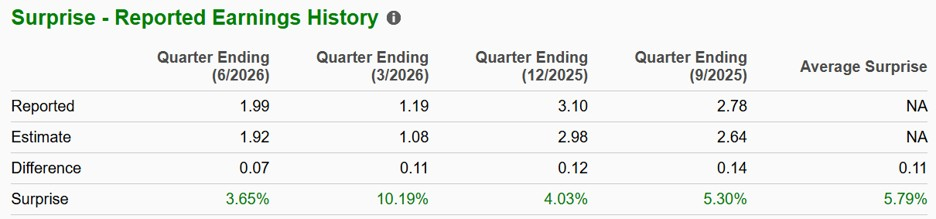

Adjusted EPS reached $1.99, comfortably ahead of expectations of $1.92 despite a dip from a quarterly peak of $3.87 per share a year ago. Still, United posted a new record in quarterly revenue as well, at $17.67 billion, which was up 16% YoY but very narrowly missed estimates.

Strong growth across premium cabins, loyalty programs, cargo operations, and international travel helped offset sharply higher fuel expenses. The company highlighted record passenger volumes while continuing to expand its global network and premium offerings.

Most impressive, United raised the low end of its full-year adjusted EPS guidance to $9.00-$11.00, up from its prior outlook of $7.00-$11.00.

Notably, United acknowledged that fuel prices remain volatile but believes stronger pricing and revenue trends should allow the airline to recover most of those higher costs over the remainder of the year.

Image Source: Zacks Investment Research

Stock Performance & Valuation Comparison (P/E)

Delighting investors is that both stocks have impressively outperformed the benchmark S&P 500 in the last three years and even the Nasdaq, although United’s gains of more than 120% have noticeably topped Delta’s 85%.

Image Source: Zacks Investment Research

Despite their strong rallies, both airlines continue to trade at valuations that offer steep discounts to the broader market.

United typically commands the lower forward earnings multiple, reflecting its more cyclical earnings profile and greater sensitivity to economic conditions.

Delta generally trades at a modest premium to United because investors have historically assigned higher multiples to its stronger balance sheet, more consistent profitability, premium revenue mix, and industry-leading operational execution.

Still, after a very extensive rally and more explosive earnings growth, United stock certainly stands out with a forward P/E of 11X compared to Delta’s 13X.

Image Source: Zacks Investment Research

Delta’s Dividend Levels The Playing Field

Income investors have a clear favorite.

Delta currently pays a dividend yielding roughly 1%, and management reinforced its confidence in future cash generation by announcing the 15% dividend increase following its Q2 report.

United, meanwhile, does not currently pay a dividend, choosing to prioritize debt reduction, aircraft investments, and strengthening its balance sheet following the pandemic.

While United may offer greater earnings leverage during favorable airline cycles, Delta remains the more appealing option for investors seeking a combination of capital appreciation and residual income.

Image Source: Zacks Investment Research

Bottom Line

Delta and United delivered impressive Q2 reports that reinforced the strength of the airline industry’s recovery despite elevated fuel costs.

For investors seeking a steadier long-term compounder with a dividend, industry-leading margins, and more predictable cash flows, Delta Air Lines appears to be the more balanced investment.

Those with a higher risk tolerance looking for stronger earnings acceleration may prefer United Airlines, particularly after management raised its full-year profit outlook.

That said, both stocks currently land a Zacks Rank #3 (Hold), although United is likely to reattain a buy rating as earnings estimate revisions should move higher in the coming weeks.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Delta Air Lines, Inc. (DAL) : Free Stock Analysis Report

United Airlines Holdings Inc (UAL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.